.png)

Act before the market

Spain counts 89,038 active online retailers, with clothes & shoes leading the category mix, an estimated +1,2bn parcels/year, and average delivery prices at €4,9 (home) vs €4,4 (OOH) for lightweight items. Our new Spain report maps the market structure, checkout dynamics, delivery methods, and how the main carriers compete for visibility - including the often-overlooked impact of white-label checkouts.

If you’re working in last-mile delivery and want a competitive view of Spain, download the full report here.

This report focuses on nine of the largest delivery providers in Spain: Correos / Correos Express, MRW, GLS, SEUR/DPD/Tipsa, DHL, NACEX, FedEx/TNT, CTT, and InPost/Mondial Relay. End-to-end retail & logistics operators (e.g., Amazon) and smaller/specialised operators (refrigerated, oversized, etc.) are intentionally excluded to keep the comparison clean and actionable.

All figures are based on Tembi’s continuous monitoring and analysis of Spanish online retailers and checkout setups, with consistent classification to support like-for-like analysis across markets. Use it to maintain competitive advantage, capture share in attractive segments, and understand market dynamics with clarity.

Quick takeaways

Spain is home to nearly 90,000 active online retailers, with a long tail that still produces meaningful parcel demand - and a smaller set of large/very large retailers that set service expectations (speed, returns, OOH availability, and delivery choice). Category-wise, Spain’s retailer base is led by clothes and shoes (~12,19%), followed by health & medicine (~7,04%) and beauty & personal care (~6,3%).

In Spain, share of presence (where a provider appears as an option in checkout) is heavily led by Correos / Correos Express, which shows up across ~41% of branded checkouts in our dataset, far ahead of the next tier (MRW, GLS, SEUR/DPD/Tipsa).

But presence is only half the story. In checkout, position matters.

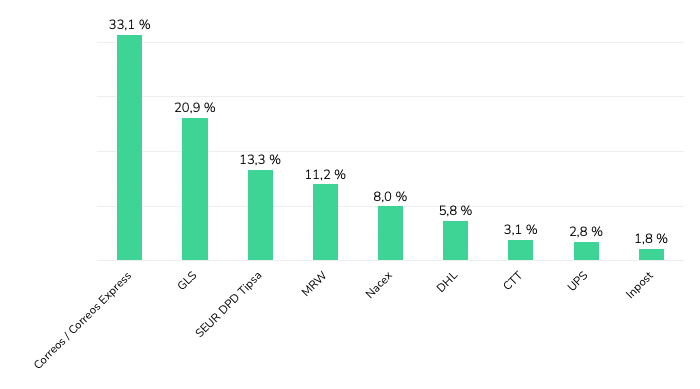

Across Spanish webshops where delivery provider brands are visible, Correos / Correos Express holds the first position most frequently (33,1%), followed by GLS (20,9%) and SEUR / DPD / Tipsa (13,3%). MRW (11,2%) and NACEX (8,0%) follow, with DHL (5,8%) and smaller shares for others.

If you read our Italy last-mile delivery analysis, you’ll recognise the same core idea: the checkout is the battlefield. The winners aren’t only those with the biggest networks - they’re the providers most consistently prioritised where consumers actually make the choice - why checkout position and visibility are a key differentiators in revenue and brand building.

Here is the uncomfortable truth for last-mile brands: a large share of Spanish retailers don’t show carrier names at all - they show only delivery methods and prices.

This matters because it means “market share” can look very different depending on whether you measure parcel volumes, merchant relationships, or brand visibility to consumers. For carriers, improving brand exposure inside white-label environments is one of the largest untapped levers in Spain - because it’s not a network problem, it’s a checkout/integration problem.

Across the market, home delivery is still the default, and the regulator view aligns with what we see in retailer setups: CNMC reports that in 2024 the usual delivery place was home (68,9%), with PUDO/convenience points (13,6%) and lockers (3,8%).

When we look at delivery methods displayed across retailers (excluding white-label checkouts), the same story holds: OOH is present, but underbuilt - especially compared to where Spain could go given consumer density and the cost-to-serve logic that OOH enables.

And pricing reinforces the direction of travel: for lightweight items, average delivery prices are roughly €4,9 (home) vs €4,3–€4,5 (OOH) depending on parcel shop vs locker. Spain is also cheaper than Italy across all options, which changes the “room” carriers have to subsidise adoption - but not the underlying incentive to densify OOH.

While retailers set the price shown in checkout, these figures consistently reflect provider positioning.

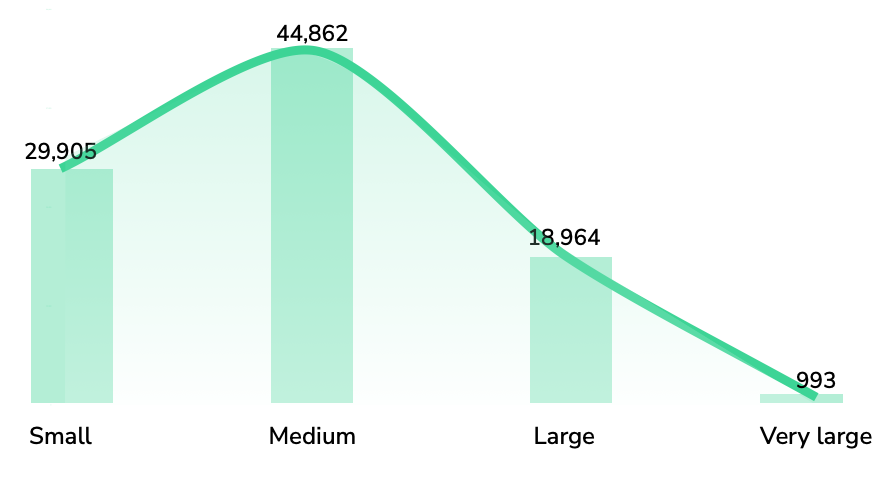

Not all “presence” is equal. The value of a provider’s retailer base depends on who those retailers are.

Using Tembi’s size scoring (0–100), we can see clear portfolio skews:

Category exposure shows the same idea from a different angle: providers aren’t just “generalists” - each ends up with a distinct category footprint (e.g., stronger concentration in health & medicine, fashion, electronics, etc.)

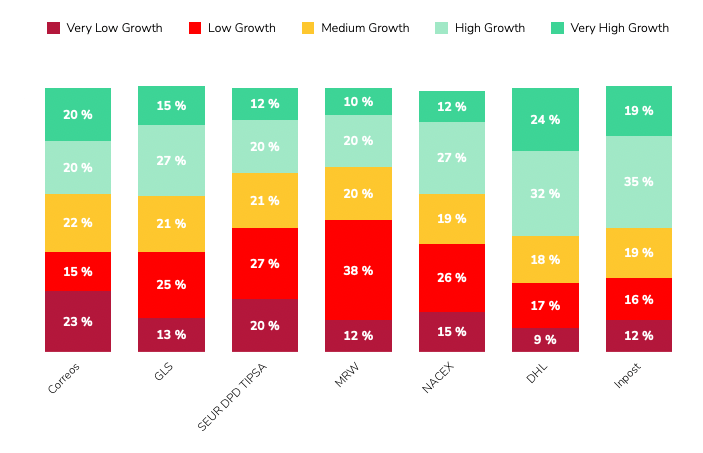

Finally, our Growth Indicator model adds a forward-looking layer: DHL and InPost have the strongest growth-weighted portfolios, with 56% and 54% of their clients forecast to be in high or very high growth bands. Correos shows a more balanced mix across growth bands.

If you want the practical “so what” for Spain, three things stand out:

Spain’s last-mile market is large, competitive, and still structurally under-optimised in checkout. Correos dominates branded presence and first-position frequency, white-label checkouts hide a big part of the market, and OOH remains a clear runway - with meaningful differences in portfolio quality and growth potential across providers.

Download the full Spain report, or schedule a Tembi demo to see your competitive landscape updated continuously across markets - including comparisons to our Italy analysis

Italy counts 94,724 online retailers, with clothing, groceries and beauty leading the mix, average home delivery cost at €6.5 and OOH at €5.8. With continued investment and InPost’s strong market entry, OOH delivery is expanding rapidly and reshaping the competitive landscape. This Italian last-mile delivery market analysis maps the structure, methods and provider portfolios behind the numbers.

Working in last-mile delivery and interested in another competitive market analysis beyond Italy? Let's connect. Download the full report here.

Italy remains one of Europe’s most active e-commerce markets by merchant count and parcel flow. To help last-mile executives benchmark strategy, this report profiles the market composition, delivery method availability and pricing, and the competitive landscape across six core providers: GLS, Poste Italiane, DPD BRT, DHL, InPost, and FedEx (TNT). You’ll see where demand concentrates by category, how pricing positions each method, and how provider client portfolios skew by retailer size and expected growth.

All figures are derived from Tembi’s continuous monitoring and analysis of Italian online retailers and checkout setups, with consistent taxonomy and normalisation to support like-for-like comparisons. Use it to maintain competitive advantage, capture share in attractive segments, and understand market dynamics with clarity.

Quick takeaways

Italy’s 94,724-strong retailer base skews to clothes & shoes (≈12.1%), then food & groceries (≈6.7%), and beauty (≈5.4%). The size pyramid shows most merchants are medium, fewer large, and about 1% very large, indicating a wide long-tail with concentrated head accounts that influence parcel mix and service expectations. The latest available data from 2020 suggest that around 830 million parcels are shipped domestically each year. Given the latest e-commerce growth estimation of an average annual growth rate of 4.5%, parcel volumes could now be approaching one billion shipments.

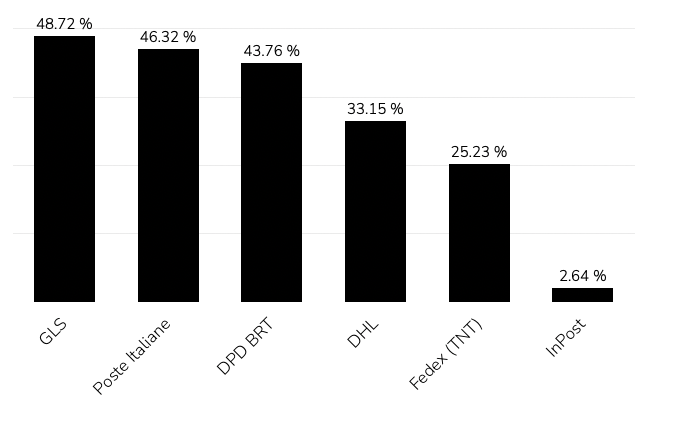

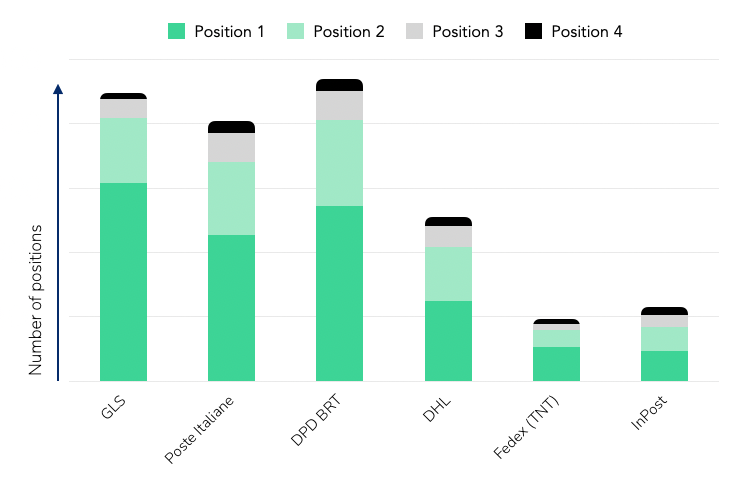

GLS and Poste Italiane hold the broadest presence across Italian webshops - GLS appears in 48.7% of retailer checkouts and Poste Italiane in 46.3%. DPD BRT, DHL, InPost, and FedEx (TNT) follow, forming the rest of the competitive landscape.

When looking at the first delivery option offered to shoppers, GLS leads with roughly 30%, followed by DPD BRT (26%) and Poste Italiane (22%).This ordering pattern reflects how retailers prioritise providers based on network reach, reliability, and negotiated terms rather than pure visibility.

In short:

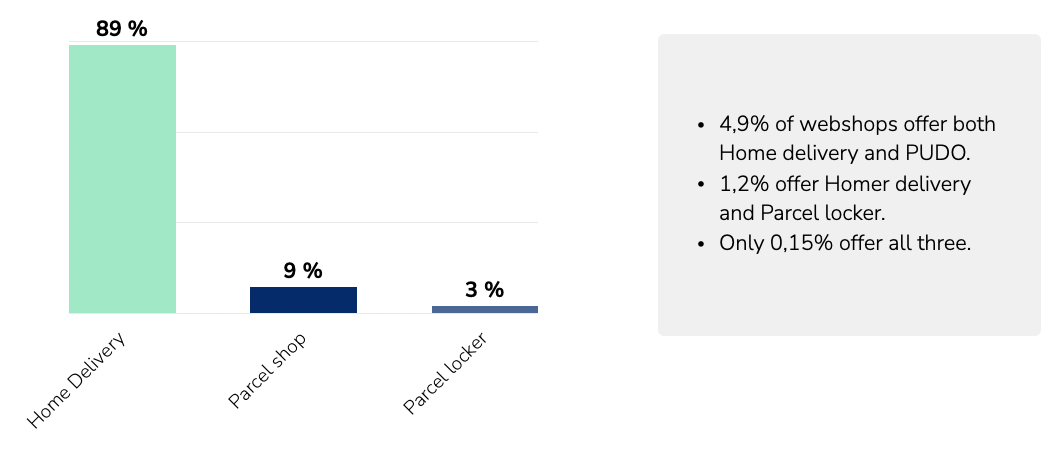

Across Italian retailers, home delivery remains dominant, offered by roughly 89% of webshops. Parcel shops (≈9%) and parcel lockers (≈3%) are still at an early stage of rollout, but both formats are expanding as networks and integrations mature.

The limited share of OOH options reflects the market’s current infrastructure capacity rather than consumer demand alone. With continued investment from providers such as InPost, Poste Italiane, and DPD BRT, OOH coverage is expected to increase steadily over the next few years, giving retailers broader flexibility in how they structure delivery choices and costs.

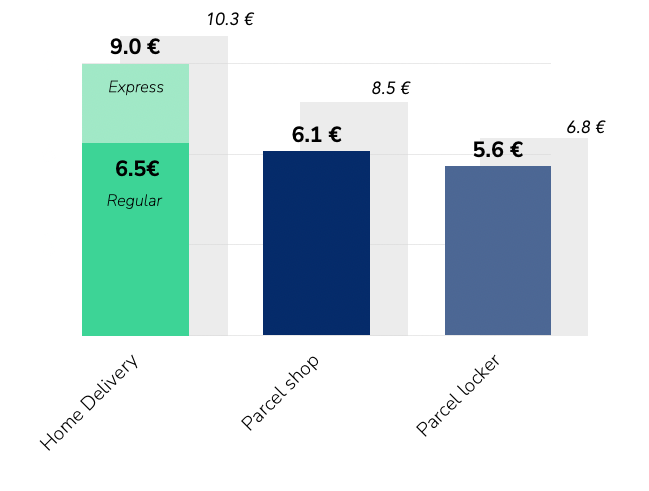

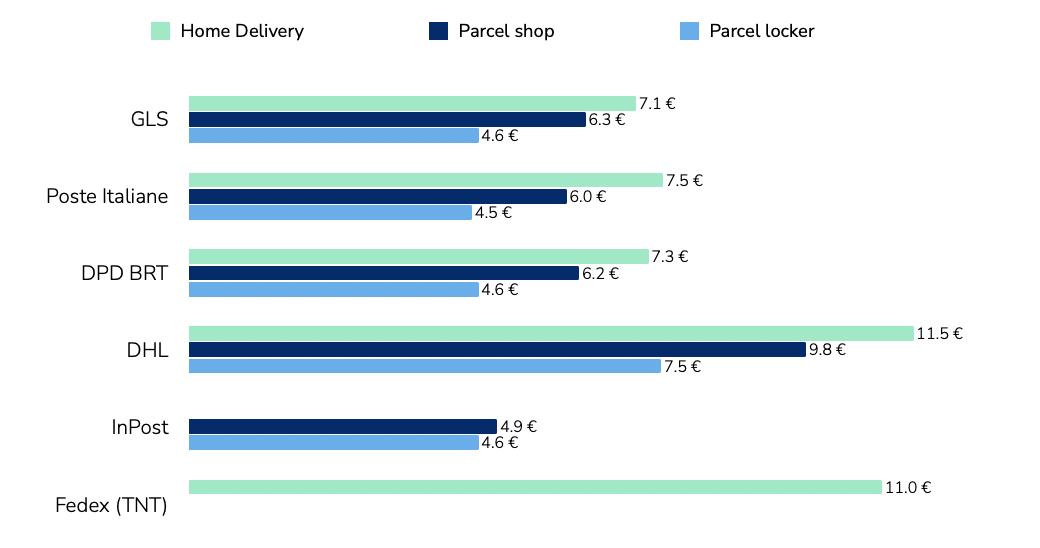

Pricing across delivery methods follows a clear hierarchy. Home delivery is the most expensive, with DHL and FedEx (TNT) positioned at the higher end in line with their express and international focus.GLS, Poste Italiane, and DPD BRT sit around the market average, reflecting large-scale domestic coverage and standardised pricing structures. InPost maintains the lowest price levels across OOH deliveries, consistent with its parcel-locker model and high network density.

The pricing gap between home and OOH - €6.5 vs €5.8 on average - highlights the economic rationale for providers to keep expanding out-of-home capacity, and in line with most other markets. As networks grow denser, these price differences will continue to influence retailer delivery mix.

Tembi’s analysis segments retailer clients by size and growth outlook, showing how each provider’s portfolio is positioned across the Italian market.

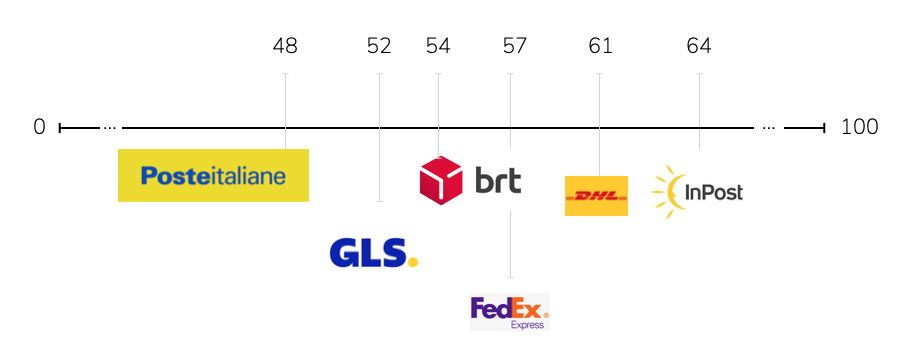

This chart summarises the average retailer size of each provider’s client base on Tembi’s 0–100 scale, where higher scores represent larger and more established webshops.

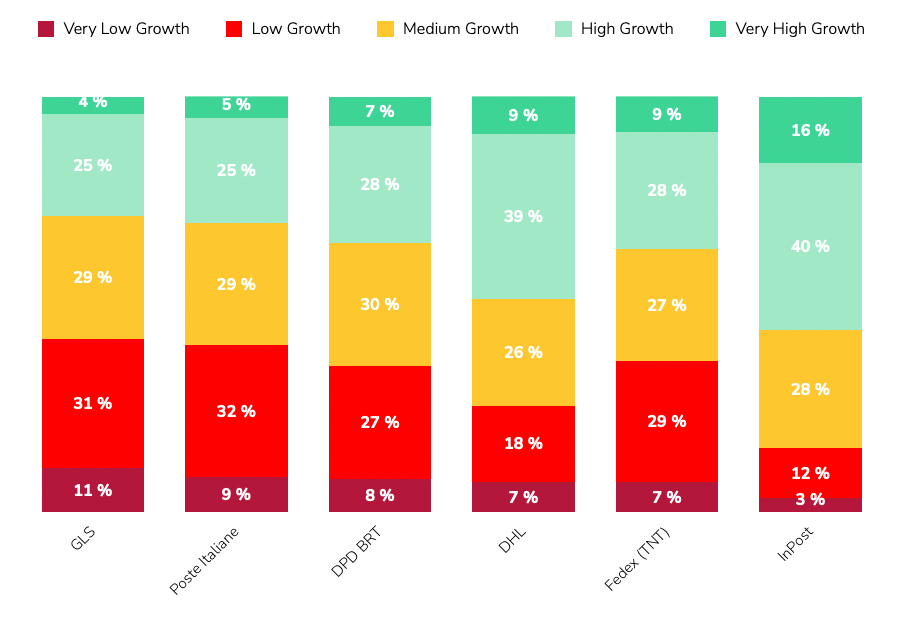

The stacked bars show how each delivery provider’s clients are distributed by retailer size:

Using Tembi’s forward-looking Growth Indicator - a composite of product portfolio development, traffic momentum, financial proxies, and export activity - InPost has the highest share of high- and very-high-growth retailers, reflecting its alignment with fast-scaling digital merchants. DHL also skews towards higher-growth segments, supported by its express and cross-border strengths. Meanwhile, GLS, Poste Italiane, and DPD BRT hold proportionally larger bases of mature retailers, providing stability and recurring parcel volume.

Locker and parcel shop networks are entering a phase of rapid expansion across Italy.InPost leads with more than 3,000 lockers installed at the start of 2025. DHL and Poste Italiane jointly reported around 500 lockers by mid-2025, alongside an ambitious plan to reach 10,000 units in the coming years. DPD BRT, through its Fermopoint network, aims for up to 4,000 lockers within five years, while GLS initiated its own rollout during 2025.

This coordinated investment places Italy on a clear multi-year OOH growth trajectory, reshaping how carriers balance cost, capacity, and customer reach. The build-out is not just a convenience upgrade; it’s a structural shift in network economics - each new locker or parcel shop reduces last-mile cost per parcel and expands delivery capacity in urban areas.

Why it matters

Rising locker and parcel shop density directly influences:

As the network matures, OOH will become a central component of Italy’s last-mile infrastructure, shaping both consumer choice and carrier efficiency.

Tembi’s analysis highlights three practical dimensions that matter for market strategy and portfolio alignment.

1. Segment by retailer size and category

Italy’s retailer landscape is dominated by small and medium merchants, but larger and premium-category retailers - such as fashion, beauty, and consumer electronics - set higher expectations for service speed, reliability, and returns. Delivery providers should align SLAs, OOH coverage, and returns management to match those standards while maintaining efficient access to the long tail.

2. Model the price–mix effect

With home delivery averaging €6.5 and OOH €5.8, even a modest shift in checkout mix can materially improve cost-to-serve for both carriers and retailers. Tracking these dynamics by category and region helps identify where OOH incentives or dynamic checkout sequencing can achieve measurable margin impact.

3. Track portfolio momentum

Provider client portfolios differ in growth exposure. InPost and DHL are more concentrated among high-growth retailers, while GLS, Poste Italiane, and DPD BRT anchor the market’s stable core. Monitoring these shifts over time helps providers balance predictable SMB volume with faster-growing digital retailers, ensuring coverage across both maturity extremes.

Italy’s last-mile market is broad, price-competitive, and evolving. Method economics continue to favour OOH expansion as networks densify; provider portfolios show divergent exposures across retailer size and growth; and the locker build-out marks a long-term structural transformation rather than a short-term initiative.

This Italian last-mile delivery market analysis outlines the market map and comparative signals needed to inform planning, benchmarking, and partnership strategies across the sector.

Download the full Italian market report or schedule a Tembi demo to see your competitive view updated continuously.

How a Last-Mile delivery commercial team used Tembi to reach online retailers when they were most likely to engage.

A last mile delivery provider was looking to improve how and when they approached new merchant prospects. While they had a solid understanding of who they wanted to work with, outreach often happened too early (before the merchant was ready to switch) or too late (after a competitor had locked in a contract).

Without visibility into what was changing in the merchant’s checkout, reps had to rely on cold outreach, hoping to catch a merchant at the right moment. They needed a way to:

Using Tembi Checkout Intelligence, the team started monitoring live changes in merchant checkout configurations. Tembi scrapers simulate checkout flows on thousands of webshops and detect:

The team set up biweekly alerts on merchants that matched their ICP and showed recent changes in their delivery stack. This created a dynamic feed of prospects likely to be re-evaluating logistics partners, so an ideal timing for outreach.

The team didn’t need to chase every webshop in a market. Instead, they focused on high-potential accounts showing signs of change. Over a six-week period, they:

Timing their approach based on real signals helped them avoid wasted effort and start conversations when interest was highest.

✅ Actionable timing signals was more effective than cold outreach

✅ Changes tracked automatically from actual checkout flows

✅ Focus on merchants in motion who are more likely to convert

✅ Fewer dead ends - reps only acted when there was a reason to reach out

A last mile delivery provider operating across several European countries needed to give its regional sales & partnerships team a clearer picture of how competing providers were positioned locally. Without reliable data, the team depended on anecdotal feedback from merchants or patchy CRM notes about which providers were in use. This made it difficult to:

• Prepare for calls with accurate competitor insight

• Spot new merchant opportunities based on delivery gaps

• Build region-specific messaging around speed, tracking, or price

They weren’t seeking a broad market expansion strategy, just precise, local visibility to sharpen commercial conversations.

Using Tembi Checkout Intelligence, the team pulled data on hundreds of webshops in their target region. Tembi’s technology visits every retailer with an active webshop and creates visibility into checkout flows and extracts structured data on:

• Which delivery providers are actually offered

• Delivery speeds and prices

• Labels and methods (e.g. express, standard, tracked) in use

• Recent changes - such as a provider being added or removed

• Images of how delivery options were presented

The data, updated every two weeks, enabled quick filtering by platform (e.g. Shopify, WooCommerce), product category, and country/area. Local sales teams gained a trusted, up-to-date view of the real delivery landscape.

With provider usage clearly mapped for their target region, the team could:

• Enter sales calls with confidence, knowing which competitor was in place

• Spot merchants lacking tracked or fast delivery options

• Tailor outreach to emphasise service gaps (e.g. slow delivery, high fees)

• Build target lists of merchants using weaker providers for displacement opportunities

No major strategic shift - just sharper conversations, better timing, and stronger commercial positioning at the local level. With a 20% increase in conversion.

• Data based on real checkout flows - not assumptions or outdated lists

• Biweekly updates kept teams working with fresh information

• Easy filtering by region and platform enabled targeted, local action

• Directly supported pre-call research, personalised outreach, and competitive mapping

Interested in exploring how Checkout Data and Webshop Monitoring can help you grow your sales? Book a call with one of our Last-mile data experts. Book a demo

Across Europe, the last-mile delivery landscape is rapidly evolving, driven by consumer preferences, sustainability pressures, and regulatory changes. Recent data from delivery providers, postal services, and consumer surveys across 13 European countries - Sweden, Denmark, Finland, Norway, Italy, the Netherlands, Slovakia, Latvia, Lithuania, Estonia, Hungary, Bulgaria, and Romania - reveals distinct regional patterns in how online purchases reach consumers.

A recent analysis from our e-commerce database, based on data from over 140,000 webshops across these countries, provides deeper insights into how extensively online retailers offer different delivery methods.

Nordic countries have strongly adopted out-of-home (OOH) delivery methods, including parcel shops and lockers. Sweden traditionally favours parcel shops, with Tembi’s data showing 36.1% of Swedish webshops offering this method. Denmark stands out with parcel shop deliveries offered by 57.6% of webshops, reflecting extensive and convenient networks.

Finland is a leader in parcel locker adoption - 34.1% of Finnish webshops offer locker delivery, supported by a widespread network of accessible 24/7 lockers. Norway balances between home (52.1% of webshops) and parcel shop deliveries (33%), with locker installations growing at 9%, indicating increasing preference for flexible, automated solutions.

Estonia, Latvia, and Lithuania showcase exceptional acceptance of parcel lockers. In Estonia, a remarkable 71.8% of webshops offer parcel lockers, validating Estonia’s leadership in locker infrastructure. Lithuania and Latvia follow closely, with 66.4% and 54.7% respectively offering parcel lockers, strongly supporting consumer preferences for convenience and reduced environmental impact.

In Western Europe, the Netherlands strongly prefers collect-yourself options, with Tembi data showing 76.4% of Dutch webshops offer this method. Home delivery remains prevalent, offered by 27.5% of retailers, aligning with the Dutch consumer's primary preference for doorstep delivery but complemented significantly by collect-yourself options.

Italy, traditionally a home-delivery market, now shows a strong adoption of collect-yourself options, offered by 64.9% of Italian webshops. Out-of-home delivery is now Italy's second most popular delivery option after home delivery, driven by convenience and reliability.

Eastern European markets like Slovakia, Hungary, Romania, and Bulgaria traditionally favoured home delivery but now rapidly integrate OOH options. Slovakia prominently features home delivery (76.9%) but also offers parcel shops through 42.9% of webshops, echoing the region's evolving preferences.

Hungary continues to favour home delivery significantly (82.6%), but parcel lockers have rapidly expanded, with about 37.7% of webshops offering this method. Romania, while strongly home-delivery oriented (83.9%), sees parcel lockers emerging as supplementary (21.2%).

Bulgaria uniquely highlights workplace delivery, offered by 36.2% of online retailers, underscoring its importance in urban logistics. This method provides practical advantages in urban areas where home deliveries may face reliability challenges.

Belgium recently mandated online retailers offer at least two delivery options at checkout, including one eco-friendly alternative such as parcel shops or lockers. Effective from 2024, this regulation aims to reduce failed deliveries, lower emissions, and encourage sustainable consumer choices (bpost, 2024). This legislative move sets a precedent that other European countries might soon follow.

Parcel lockers and out-of-home delivery significantly reduce last-mile delivery emissions, potentially cutting CO₂ by approximately 30% compared to home delivery, especially when consumers collect parcels using sustainable transport methods (McKinsey, 2024). Dense networks of lockers and collection points, common in Estonia, Finland, and the Netherlands, enhance urban delivery efficiency, reduce traffic congestion, and improve consumer satisfaction.

European last-mile delivery is undeniably trending towards flexible, sustainable methods that reflect varied regional consumer behaviours. As OOH options mature and consumer awareness grows, home delivery will increasingly coexist with alternative methods. Carriers and retailers who proactively adapt will lead in delivering not just parcels, but also consumer satisfaction and sustainability.

Our recent analysis of aggregated data from webshops in selected European countries confirms two straightforward insights about cross-border selling: webshops typically target neighbouring countries or seek out larger markets to grow their potential customer base. While these findings may seem intuitive, the data illustrates clearly how consistently webshops employ these strategies - particularly when supported by strong partnerships with local logistics providers and prioritised investments in localisation.

The obvious role of proximity

Webshops in Denmark primarily target Sweden (18.9%) and Germany (18%), reflecting straightforward cross-border logistics and cultural familiarity. Similarly, Dutch webshops predominantly sell to Belgium (17.4%) and Germany (13.5%), confirming that short distances and established regional logistics make neighbouring countries natural first choices. Swedish webshops follow the same logic, favouring close neighbours Denmark (17.2%) and Finland (15.9%).

Targeting larger markets beyond proximity

Webshops strategically pursue larger markets with robust consumer bases, such as Germany and France, regardless of direct proximity. For instance, Italian webshops commonly sell to Germany (14.2%) and France (14.1%), driven significantly by the size and high purchasing power of these markets, alongside geographical closeness.

Distinctive patterns in Eastern Europe

Webshops in Hungary display notably low cross-border priority: only 4.4% offer shipping options to Germany, Slovakia, and Romania. This cautious approach likely reflects specific economic calculations, infrastructural limitations, or less developed cross-border logistics partnerships, rather than purely geographical factors.

Latvian webshops clearly illustrate the proximity factor again, heavily targeting neighbouring Lithuania (16.8%) and Estonia (15.9%), highlighting ease of trade through geographic and cultural closeness.

Notable differences in cross-border engagement levels

A significant finding from the data is the variation in how actively webshops pursue international markets. Factors driving these differences include the maturity of the domestic e-commerce market, logistical infrastructure, consumer purchasing power, and particularly the level of investment into localisation and logistics solutions. Engagement levels notably decline with increasing distance, indicating logistical complexity and higher costs likely deter webshops from extensive international expansion beyond neighbouring or well-established larger markets.

Concluding remarks

Our aggregated data confirms proximity and market size as primary drivers for cross-border e-commerce decisions. However, the diverse patterns and varying engagement levels suggest that webshop decisions are influenced by more complex strategic factors, including infrastructural readiness, economic conditions, logistical capabilities, and the willingness to invest in localised consumer experiences. These factors ultimately shape cross-border success far more than geographical closeness alone.

Last‑mile delivery shapes the online shopping experience, influencing conversion rates, repeat purchases and brand perception.

At Tembi, we analysed over 600,000 webshops to understand two aspects of last‑mile competition in 17 European markets, the market share of the top delivery provider and the number of distinct delivery partners each webshop integrates, and how these factors drive innovation and strategy.

Rather than estimating parcel volumes, we examined the presence of delivery providers in webshop back‑ends. Every integration represents a commitment by the webshop to offer that carrier at checkout. By counting integrations, we capture:

• Breadth of choice available to consumers

• Carrier prominence within each market

For each country - from Belgium to Slovakia - we identified the top three providers by share of webshop integrations and counted the total number of providers in active use. We excluded providers that have less than 1% market presence.

These figures show that while national postal services still lead in many markets, no single carrier dominates everywhere, and the number of options ranges from three providers in Iceland to more than twenty in the Netherlands.

We classify markets by the checkout presence held by the leading provider:

Adding the count of distinct delivery partners shows where compeition is the hightst:

Most fragmented markets, such as the Netherlands, Romania and Sweden, offer webshops a broad selection of carriers to tailor delivery options by region, price‑point and service level. In the Netherlands, for instance, there are over twenty distinct last‑mile providers active across the market. By contrast, in Iceland and Bulgaria webshops have fewer providers to choose from, simplifying management but concentrating risk, and less consumer choice. Finland sits between these extremes, with around fourteen partners in use yet Posti being present in 62% of all webshop checkouts.

Geography plays a crucial role in shaping last‑mile dynamics. In countries with vast rural areas and archipelagos - most notably Finland and Sweden - webshops need delivery partners that can reliably serve both remote villages and dense urban centres. National posts excel at this: Posti’s 62 percent presence in Finland and PostNord’s 33 percent in Sweden reflect their ability to cover every corner of the country, from Lapland to the Helsinki suburbs, or from the Stockholm archipelago to the far north. This extensive network cements their leadership and makes it challenging for smaller couriers to compete on a truly national scale.

At the same time, urban populations in these markets demand faster and more flexible options. That’s why even highly consolidated markets like Finland still see around fourteen delivery partners in use, and Sweden nearly eighteen. Specialist providers focus on city‑centre same‑day deliveries, parcel locker networks and niche eco‑services, carving out space alongside the national postal incumbent.

By contrast, in highly fragmented markets such as the Netherlands, Italy and Romania, geography is less of a barrier - population density is higher and distances shorter - so webshops routinely offer 18 to 22 different providers to meet varied consumer preferences. National posts such as PostNL and Poste Italiane must innovate continually, rolling out premium services like carbon‑neutral shipping, click‑and‑collect lockers and advanced tracking, and partnering with crowd‑shipping or on‑demand couriers to fill gaps.

In moderately consolidated markets - Denmark, Belgium, Switzerland and the Baltics - the mix reflects mid‑range geography and market size. National posts share the stage with regional specialists (such as GLS and DPD), driving innovation in service differentiation, tech integration and sustainability (electric fleets, bike couriers, offset programmes).

Finally, in smaller or more remote markets like Iceland and Bulgaria, webshops often layer core postal services with a handful (three to five) of local same‑day or on‑demand couriers to ensure coverage. Even here, national posts are expanding parcel‑locker footprints and app‑based tracking to meet rising consumer expectations - while keeping a watchful eye towards rapidly growing new digital-first ventures.

Understanding these overlapping factors - market consolidation, provider fragmentation and geographic realities - allows e‑commerce leaders to tailor last‑mile strategies. In widespread, low‑density regions, deep partnerships with national posts ensure full coverage; in dense, competitive markets, robust multi‑carrier technology and innovative niche services deliver the flexibility consumers expect.

Stay tuned for more insights and sign-up to our monthly newsletter.

or e-commerce consumers, delivery costs often represent the final hurdle before completing a purchase. Set too high, delivery fees can drive potential buyers away; priced competitively, they can boost conversions and foster customer loyalty. At Tembi, we closely track these shifts, monitoring what webshops across Europe charge consumers for different delivery methods.

We analysed webshop delivery pricing data across nine markets from October 2024 to March 2025, examining variations across three key delivery methods: parcel box, parcel shop, and home delivery.

Over 300.000 webshops are part of this analysis and we've removed the outliers when calculatin average deliver prices (free delivery and delivery of large and/or heavy objects).

%403x.jpg)

Parcel boxes have become a popular choice due to convenience and lower operational costs. However, pricing varied significantly:

Parcel shops offer flexibility for consumers who prefer to pick up orders at convenient locations:

Home delivery remains the premium service and is generally priced highest:

These shifts in delivery prices reveal strategic decisions by webshops rather than direct changes in logistics provider pricing. Webshops balance several factors:

For commercial leaders in e-commerce, understanding these pricing strategies is critical. Lower delivery prices may indicate aggressive market positioning or efficiency gains, while increases might signal tighter operational conditions or reduced competition.

Webshop delivery pricing is a powerful indicator of market conditions and consumer expectations. Regular monitoring of these shifts is essential to stay competitive and agile - regardless if you're a retailer selling directrly or inderictly, or operate a last-mile delivery provider.

s we approach the year's final quarter, the stakes for last-mile delivery companies couldn't be higher. With the majority of revenue generated from B2C webshops, Black Friday, Cyber Monday, and the Christmas season represent crucial opportunities to maximise profits.

However, preparation for these peak periods involves more than ramping up staff, fine-tuning routing, and increasing throughput.

At Tembi, having helped over 40 last-mile providers across Europe, we understand that strategic planning on the commercial side can make or break your Q4 performance. To help you in the process we have collected a five of our key learnings on the topic.

Instead of focusing solely on acquiring new clients, ensure you're optimally positioned with your existing ones. Monitoring your position in their checkout process can yield significant returns. Being positioned as the top delivery provider at the delivery checkout can dramatically increase the number of orders you receive, often doubling or even tripling them.

From several of our Last-mile delivery clients, we have witnessed an average of 30%-50% increase in top-1 rankings working tactically with this. Typically, this amounts to a total increase of 20%- 33% in revenue from the existing client base!

Strategic client acquisition is essential. Focus on attracting webshops that boast a strong infrastructure, high order volumes, and the right geographical locations that align with your logistics.

These targeted efforts can significantly enhance your profit margins and operational efficiency.

On the other hand, failing to identify the clients that are right for you means losing time and money on unsuccessful outreach, attending irrelevant meetings, and seeing your closing rate decline. And even worse, potentially attracting a non-profitable client for your business.

Market research or a good market insight & sales intelligence tool will help ensuring you target the right clients. More is not always better.

Understand where you stand out compared to your competitors and highlight your unique selling points to differentiate yourself in a crowded market. Are your delivery times faster? Do you offer more sustainable options? Is your service reliability superior?

Tembi’s E-commerce Market Intelligence solution provides users with a comprehensive, data-driven market overview. This enables last-mile delivery companies to understand their performance and how they measure up against competitors. Our data not only visualises your strengths but also serves as credible evidence of your advantages.

Combining this data with comprehensive insights into each webshop in your market provides a significant advantage in sales meetings. You can tailor your pitch using up-to-date information, demonstrating how your solution will enhance the delivery experience for your customers' clients. This personalised approach showcases the specific benefits and improvements your service offers, making a compelling case for why your company is the best choice.

Q4 is a vulnerable time for webshops, where faulty shipments and slow deliveries can be extremely costly. Success often stems from a partnership approach between webshops and last-mile providers.

Engage deeply with your clients to ensure they see you as a trusted partner they can rely on during these critical periods.

In essence, this is where you want your sales and account management team to spend the majority of their time, which can be enabled by strong processes and the right tools/technologies to help your team be even more efficient.

Effective planning and execution require time, structured outreach, and meticulous account management. There is no easy way. The sooner you start, the better positioned you'll be to capitalise on the high season's opportunities. The time is now – not in October.

At Tembi, we bring years of experience in delivering market insights and partnership services that drive success.

Our market intelligence solutions provide last-mile delivery companies with continuously updated data and insights into webshops, delivery provider rankings, export markets, technology usage, product categories, and much more - allowing companies to react swiftly to changes, maintain top rankings, and increase revenue from their existing client base.

We tailor our supportive services to each client's needs, and we would love nothing more than to set up a free, non-committal session to discover how our e-commerce market intelligence solution could help your business achieve its revenue goals—both in Q4 and throughout the year.

iscover data and insight around webshops in Sweden, Denmark, Finland & Norway. This report is free and available on LinkedIn for download.

We've visited and analysed over 70.000 active webshops in Sweden, Denmark, Finland & Norway. Orginsed around three topics you'll find:

➜ Insights around distribution of product categories

➜ Data on delivery prices and delivery methods

➜ Discover which technology platforms power the webshops

And much more ⏩

Go to our linkedIn page and view, or download your copy.

Baltic E-Commerce Market Intelligence Report (Published January 2024)

Nordic e-commerce Market Intelligence Report (Published October 2023)