European online payments are shaped by a mix of global platforms and strong local preferences. Below we break down the key payment providers across eight countries – Belgium, Switzerland, Denmark, Finland, Italy, Norway, and Sweden – highlighting who’s active in each market, how they fare in B2B vs B2C, and domestic vs cross-border trends. We also discuss how platform-native solutions (like Shopify Payments and PayPal integrations) enable cross-market reach.

The analysis is based on 208.035 webshops monitored by Tembi with data from the 21st of May 2025.

Belgium - 18.237 active webshops

Switzerland - 30.007

Denmark - 32.370

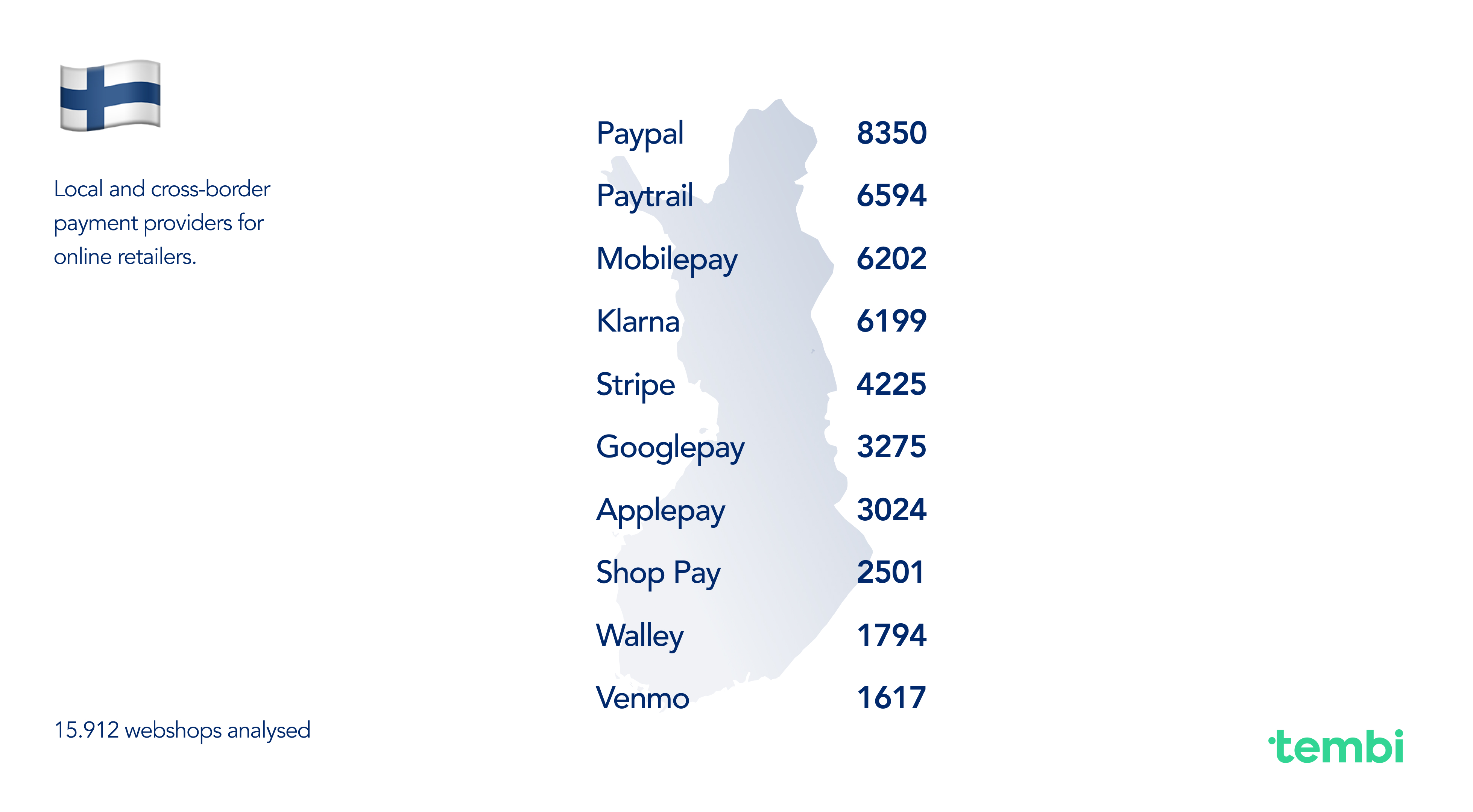

Finland - 15.912

Italy - 63.672

Norway - 15.032

Sweden - 32.805

Belgium - Bancontact’s home turf, with PayPal for cross-border

Belgian e-commerce is dominated by Bancontact, the national debit scheme, which remains by far the favourite online payment method – about 73% of Belgian shoppers prefer Bancontact and 70% use it most often (retaildetail.eu). Credit cards, once top, now take a secondary role mainly for higher-value purchases (pay.com.)

Key Providers and Roles:

- Bancontact – Ubiquitous in Belgium. Linked to virtually all Belgian banks, it has more cards in circulation than there are Belgian residents (pay.com). Merchants rely on Bancontact for its wide user base and low fraud (transactions are irrevocable once confirmed, reducing chargebacks (pay.com). It’s essentially mandatory for domestic webshops to support Bancontact.

- PayPal – While not a domestic method, PayPal is integrated into many Belgian shops (our dataset shows it on a similar number of sites as Bancontact). Its strength is in cross-border shopping: 72% of Belgians have used PayPal to buy from foreign retailers (pay.com), leveraging its buyer protection and global acceptance. PayPal thus complements Bancontact by enabling international B2C sales.

- Local Banking Apps – Major banks offer their own payment buttons (e.g. Belfius Pay), though these see modest adoption compared to Bancontact (e.g. Belfius appears on a few thousand sites). They cater to customers of those banks for bank-transfer payments.

- Global Wallets (Apple Pay, Google Pay) – Gaining presence as smartphone usage grows. Apple Pay is supported by many Belgian banks, tapping into the country’s large iPhone user base (pay.com.. These wallets remain convenience add-ons rather than primary methods, but their acceptance in Belgian webshops (thousands of sites) signals a growing cross-platform trend.

- International PSPs (Stripe, Mollie) – Providers like Stripe and Dutch-based Mollie are used by Belgian merchants (Mollie has ~4,500 Belgian sites in our data). They enable credit cards and alternative methods easily, including Bancontact itself via their integration. This is especially useful for smaller B2B merchants expanding online, as PSPs handle multi-method support in one package.

Domestic vs international adoption

Domestically, a Belgian online shopper expects to see Bancontact at checkout – it’s a trust signal and caters to local payment habits. International e-commerce players entering Belgium must integrate Bancontact (often via Shopify Payments or Adyen) to localise their offering (retaildetail.eu). Conversely, Belgian merchants aiming cross-border include methods like PayPal and credit cards to accommodate foreign customers who can’t use Bancontact. Thus, Belgian sites serving neighboring markets often support both local and global methods. This dual approach (Bancontact + an international wallet) is common in Belgium’s e-commerce, ensuring both local and cross-border sales are covered.

Switzerland - Twint charging up

Switzerland’s payment mix is unusually diverse. Traditionally, bank transfers and invoices have been extremely popular – as of 2023, bank transfers (including pay-by-invoice) were projected to account for ~46% of Swiss e-commerce transactions (pay.com) Cards are also widely used (52% of online transactions, mostly credit cards in online contexts (pay.com). But the biggest shake-up has come from Twint, the Swiss mobile payments app. In recent years Twint has surged to become the dominant online payment method: it’s now accepted in roughly 4 out of 5 Swiss online shops (twint.ch) and counts over 5 million active users in a country of ~8.7 million (pay.com).

Key Providers and Roles:

- TWINT – A home-grown mobile wallet linked to users’ bank accounts. Launched in 2016 by major Swiss banks, Twint has achieved 98% brand awareness and massive uptake (fintechnews.ch). It’s used for instant bank-direct payments via app (often by scanning a QR code). By 2022, about 74% of Swiss online merchants supported Twint (fintechnews.ch), and that share is still rising (Twint itself boasts ~80% online shop coverage (twint.ch). For domestic B2C, Twint’s appeal is convenience and local trust – it effectively modernized the traditional bank transfer for the mobile era.

- Credit & Debit Cards – Swiss consumers use cards frequently, especially credit cards for online shopping (an estimated 80% of Swiss prefer credit over debit for e-commerce)pay.com. Visa and Mastercard dominate (around 64% and 17% market share respectively in cards)pay.com, with PostFinance (the postal bank’s debit card) filling much of the remainder domestically. PostFinance’s payment option (e-finance or card) is offered by many Swiss shops (our data shows it on ~5,700 sites) to cater to the large customer base of the national postal bank. Cards are important for both B2C and B2B (corporate cards, etc.), though Swiss B2B buyers sometimes still prefer invoice.

- Bank Transfers & Invoicing – A significant share of Swiss e-commerce is essentially “pay after delivery.” Many Swiss shoppers choose to receive an invoice (often with a QR-bill) and pay it via their e-banking – this shows up in stats as bank transfer payments. Even online, merchants often offer “purchase on account.” Providers like Klarna have entered Switzerland to offer pay-later, but the concept was already ingrained. Sofort (Klarna’s direct bank transfer service) also appears in Swiss webshops (in ~12k of them per our data) as a popular option for real-time bank payments, used especially for cross-border transactions with Germany.

- PayPal – PayPal enjoys steady use in Switzerland, but it’s not as dominant as in some other countries. It’s present on most international-facing Swiss shops and is popular for cross-border purchases or niche uses. Swiss consumers do use PayPal domestically, but with Twint and cards readily available, PayPal’s role is more as a universal fallback. Still, our scan found PayPal on ~22,600 Swiss sites – the single most common payment brand on Swiss shops – underscoring its broad presence even if volume share is smaller.

- Local Banking Options – Apart from Twint, Swiss merchants may support one-click bank payment through services like eBill or direct debit for B2B, but these are less visible. Revolut’s new checkout option has also cropped up (around 4k sites) as Switzerland has many Revolut users; this is mainly to serve tech-savvy shoppers and cross-border customers with Revolut accounts.

Domestic vs international

The Swiss market is small but high-spending, and cross-border e-commerce is significant (many Swiss buy from German, French, or global sites). Domestic shops therefore try to offer a mix of local and international methods. For instance, a Swiss webshop will almost certainly offer Twint and PostFinance for locals, but also Visa/Mastercard and PayPal to appeal to everyone (including cross-border shoppers or expatriates). International retailers entering Switzerland often integrate Twint now – given its reach, not having Twint could alienate a big chunk of local customers. At the same time, Swiss consumers use credit cards and PayPal especially when shopping on foreign sites, since those universally work. This dynamic means successful cross-border sellers into Switzerland either enable local methods via a PSP (Adyen, etc.) or rely on the Swiss buyer falling back to a credit card or PayPal. In summary, Swiss e-commerce shows a dual nature: traditional methods (bank transfer/invoice) remain very strong at home (pay.com), but mobile and global solutions are rapidly overlaying to facilitate seamless buying both domestically and across borders.

Denmark - Home of MobilePay

Denmark is a card-centric country with a twist – nearly every Dane has a Dankort (the national debit card, typically co-branded with Visa), so card payments have long been the norm. In 2024, about 37% of Danish online consumers cited paying by card as their primary method (ecommercenews.eu). Close on its heels, however, is MobilePay, used by roughly 33% of online shoppers as their preferred option (ecommercenews.eu). MobilePay, a mobile wallet linked to card or bank accounts, has become nearly ubiquitous (over 90% of Danes have the app, and virtually all younger adults do (statista.com)). PayPal and other methods exist but are less prominent – a few years ago PayPal accounted for ~13% of Danish online payments (oosga.com), and it remains a common option particularly for cross-border purchases. Overall, Denmark’s landscape mixes global card infrastructure with highly adopted local fintech solutions.

Key Providers and Roles:

- Dankort / Card Payments – Debit/credit cards are still the #1 online payment method in Denmark by usage (ecommercenews.eu). The Danish Dankort (often used via Visa rails online) ensures almost anyone with a bank account can pay by card. Merchants benefit from well-established card processing and Danes’ comfort with cards for larger or recurring purchases. International cards (Visa, Mastercard) are widely accepted, which also covers foreign shoppers. For B2B e-commerce, cards (corporate cards) are common too.

- MobilePay – Denmark’s signature mobile wallet app. MobilePay allows one-click or app-confirmation payments drawing funds from the user’s card or bank. It’s deeply ingrained in daily life; in e-commerce it’s become the convenient alternative to entering card details. With 33%+ share of online payments and growing (ecommercenews.eu), MobilePay is almost expected on Danish sites – from small boutiques to large retailers. For merchants, offering MobilePay can boost checkout conversion on mobile devices. Notably, MobilePay is popular in B2C contexts (fast checkout for consumers), while in B2B it’s used less (business buyers typically use cards or invoices).

- PayPal – Widely available, though not top-of-mind for Danes domestically. Many Danish webshops include PayPal, especially those on platforms like WooCommerce/Shopify where it’s an easy plug-in. It serves mainly as a way to accept payments from international customers or cater to Danes who already have PayPal accounts. While only about 13% of Danish e-commerce shoppers used PayPal as of 2021 (oosga.com), it remains a useful cross-border channel – for example, Danes buying from eBay or foreign sites often use PayPal.

- Local PSPs (Payment Service Providers) – Denmark has a robust set of payment gateways that serve merchants. QuickPay and OnPay are examples of Danish PSPs that many webshops use behind the scenes. These providers bundle various methods (cards, MobilePay, Viabill, etc.) and are particularly important for SMEs and B2B shops, as they handle the integrations and local acquiring. In our data, QuickPay appears on ~4,800 sites, indicating its strong presence. Such PSPs typically don’t matter to the consumer (who just sees the payment options they provide), but they are key enablers of the local payment ecosystem.

- Buy Now, Pay Later and Others – Danes have access to BNPL options like ViaBill or Klarna, but uptake is more moderate compared to Sweden or Norway. Klarna is integrated in some Danish shops (~6,600 sites in our scan) targeting installment payments for consumers. However, Danish shoppers, being comfortable with cards, haven’t embraced BNPL to the same extent as Swedes. For B2B, offering payment on invoice is common (especially when selling to government or large companies, who use EAN invoicing), though that’s handled outside the online checkout or via invoicing services rather than through visible providers in checkout.

Domestic vs International Adoption

Danish online retailers focus on domestic preferences first – supporting Dankort/Visa and MobilePay to cover the vast majority of local transactions. Cross-border, Denmark has a high rate of consumers buying from abroad (over half shop abroad monthly (ecommercenews.eu), so Danish merchants also consider methods that international shoppers use. This means accepting foreign Visa/Mastercards (no problem via standard acquiring) and often keeping PayPal available. International merchants selling into Denmark are wise to enable MobilePay – increasingly, payment platforms (like Stripe or Adyen or Shopify Payments) let them do so easily. We see that cross-border giants (Amazon, etc.) have started to include MobilePay for Danish customers. In summary, domestic Danish e-commerce is characterised by card and MobilePay dominance, whereas cross-border commerce relies more on international card networks and PayPal – but the gap is closing as local methods become accessible to foreign merchants too.

Finland: Paytrail dominates

Finnish online shoppers have a strong preference for direct bank payments. Rather than using individual bank buttons, Finland streamlined this through Paytrail, an aggregator that connects all major Finnish banks. As a result, online bank transfer solutions like Paytrail are the top choice for Finns (aboutpayments.com). According to industry info, Finnish consumers most prefer paying via their internet banking through services such as Paytrail or Trustly (aboutpayments.com). Cards are of course used as well, but historically Finland has seen lower credit card usage online than many other European countries. Instead, debit cards via bank transfer and recently mobile wallets are prominent. MobilePay (imported from Denmark) has also gained traction in Finland – it’s available and used by many, though not yet as dominant as in Denmark. Klarna is popular in Finland too (Finland was an early Klarna expansion market), and invoice payments are fairly common for certain purchases. In summary, Finland’s payment scene is a mix of bank-centric methods and a few select international options.

Key Providers and Roles:

- Paytrail – Arguably the backbone of Finnish e-commerce payments. Paytrail (now part of the Nets/Nexi group) offers merchants a single contract to accept all Finnish online banking payments, cards, as well as local wallets and invoices (nexigroup.com). It is the most used online payment service in Finland’s e-commerce (mastercard.com), which aligns with our data where Paytrail appears very frequently (over 6,500 Finnish sites). For consumers, Paytrail provides a seamless interface to pay from any Finnish bank account, which is highly trusted and convenient. In practice, when a Finnish shopper chooses “online bank payment,” it’s often Paytrail processing it in the background. This method is equally relevant for B2C and B2B – businesses also appreciate paying directly from bank accounts.

- Trustly – Another bank transfer option, used in Finland and across the Nordics. Trustly allows instant bank payments without leaving the merchant’s site. Finnish shoppers do use Trustly, but since Paytrail already covers domestic banks, Trustly’s role is more for cross-border scenarios (e.g. paying from a Finnish bank on a foreign site). Still, it’s noted as a top method after Paytrai (aboutpayments.com). Some Finnish merchants include Trustly in addition to Paytrail to capture every preference.

- Cards (Visa/MasterCard) – International debit/credit cards are widely accepted and come next in popularity after bank transfers for Finns (aboutpayments.com). Finland historically had a strong culture of paying by bank rather than credit, but card usage is rising. Most Finnish cards are debit or dual-function cards, and many are used via Paytrail’s interface or via a PSP like Nets/Paytrail itself. For the merchant, accepting cards is essential for cross-border customers and for those Finnish buyers who prefer a familiar Visa/Mastercard flow or need to use a credit line.

- Klarna – Finland is one of Klarna’s significant markets. Klarna’s pay-later and installment options are offered by a lot of Finnish online stores (our data shows Klarna on ~6,200 Finnish sites, nearly equal to MobilePay’s presence). Finnish consumers use Klarna mainly for splitting payments or buying on invoice, similar to Sweden but perhaps slightly less intensively. It’s a popular option for B2C retail (fashion, electronics – where try-before-you-buy or installment plans appeal). For merchants, Klarna brings potential conversion gains and is often included alongside traditional methods. In B2B sales, Klarna is not commonly used – Finnish businesses would use direct invoicing if they want post-payment.

- MobilePay – Finland adopted MobilePay after Denmark (Danske Bank introduced it). Today, MobilePay is a commonly used wallet in Finland (aboutpayments.com), though its usage (by share of transactions) isn’t as high as in Denmark. Still, many Finnish shops (over 6,200 in our analysis) offer MobilePay at checkout. It’s popular for its ease on mobile devices and is used predominantly in B2C contexts (e.g. a consumer buying event tickets or clothes may opt for MobilePay instead of typing card details). With MobilePay’s merger with Vipps/Swish underway, Finns may see even more features, but already the app is a key part of the payments mix.

- Other Local Pay-Later (Walley, etc.) – Finland has some specialized providers like Walley (formerly Collector Bank’s solution). Walley offers invoice and installment payments, including B2B invoicing solutions. It appears in Finnish e-commerce (about 1,800 sites in our data) as an option to “Pay by invoice 14 days” or similar, often under the Walley brand in checkout. This indicates a demand especially in B2B and larger consumer purchases for invoice-based payment. Similarly, Svea (a Swedish company but active in Finland) provides B2B financing and appears on some sites. These are important for B2B e-commerce or high-value consumer sales (furniture, machinery, etc.), where customers expect to be billed or finance the purchase rather than pay upfront.

Domestic vs International

Finnish e-commerce is quite domestic-focused in method – a Finnish shopper expects to pay through their bank or an invoice. International merchants expanding to Finland often partner with Paytrail or a similar PSP to offer localized bank payments, because without those, they’d miss a large portion of sales. The prevalence of English-speaking Finns means many do shop on international sites, where they might then use a credit card or PayPal if Finnish bank options aren’t available. Indeed, PayPal is accepted on many Finnish sites (though not top-five in preference, it’s present on ~8,300 Finnish webshops per our data), functioning as a catch-all for cross-border transactions (e.g. paying a non-Finnish merchant). Adoption trends show that methods like Paytrail keep domestic transactions flowing in local currency and language, whereas global platforms like PayPal or card networks come into play for cross-border. Additionally, Finland being in the Eurozone makes cross-border shopping easier (no currency swap issues), so credit cards are slightly more used for EU-wide shopping. Finnish merchants, to expand abroad, will lean on PSPs that support international cards, PayPal, and possibly multi-currency – many use Stripe (found on ~4,200 Finnish sites) or Adyen for that reason. In sum, Finland has a strong local backbone (bank payments) that any entrant must integrate, and a willingness to layer global methods on top for broader reach.

Italy: PayPal’s Stronghold

Local Payment Landscape: Italy stands out for the prominence of PayPal in e-commerce. Italians have historically been cautious about online payments, leading them to gravitate towards PayPal for its perceived safety and buyer protection. Recent surveys show about 63% of Italian online consumers used PayPal in the past month, and 39% prefer PayPal over any other method – making it the #1 choice by far (rapyd.net). Credit and debit cards are of course used (especially with the widespread CartaSi/VISA and MasterCard), but only ~11% of Italians picked credit cards as their first choice, according to the same study (rapyd.net). Interestingly, a uniquely Italian method, the PostePay prepaid card (issued by the postal service), ranks high – about 12% choose it as their top payment method (rapyd.net). PostePay is essentially a reloadable Visa/Mastercard, and its popularity reflects Italians’ preference for controlled, cash-loaded spending. Cash on delivery (contrassegno) still lingers as an option in Italy for some categories, though its share is decreasing as digital payments grow. Overall, Italy’s online payment mix is a blend of global wallets, card networks (often through domestic brands like CartaSi or PostePay), and some remaining traditional methods.

Key Providers and Roles:

- PayPal – The undisputed leader in Italian e-commerce payments. PayPal’s ubiquity is evident: it is integrated into the vast majority of Italian webshops (our dataset found it on ~56,000 sites, far more than any other provider in Italy). Its strengths – buyer protection, ease of use, and not requiring the buyer to expose card details – resonated strongly with Italian consumers who had security concerns. Many Italians also keep balances in PayPal or link it to bank accounts, using it almost like a bank alternative. For merchants, offering PayPal is almost a must for B2C, as not having it could mean losing a huge chunk of potential customers. Even in P2B (consumer-to-business) scenarios like freelance services or marketplace sales, PayPal is common. In B2B, PayPal is less used for large transactions, but small business services sometimes get paid via PayPal too. Notably, Italian merchants rely on PayPal not just domestically but to sell internationally – it’s a ready-made cross-border solution that handles multiple currencies and languages, which helped many Italian small businesses to reach global customers.

- Credit/Debit Cards (CartaSi, Visa, Mastercard) – Card payments in Italy have grown but still face competition from PayPal and cash. Most online card usage is via Visa or Mastercard-branded cards, often issued as CartaSi (the domestic scheme, now Nexi) or as bank cards. Also, PostePay cards (Visa Electron/prepaid) are massively used by younger and unbanked consumers for online shopping. This means that while “card” as a category is significant, many Italians use them through intermediaries (like linking a PostePay to PayPal, or using the card via an Apple Pay wallet). For merchants, enabling card payments is standard – usually through PSPs like Nexi, Gestpay, Stripe, or international acquirers. However, due to high PayPal use, sometimes cards are effectively the secondary option on many sites. In B2B e-commerce, corporate credit cards are used for convenience (especially for SMEs buying software, travel, etc.), but larger purchases often go through bank transfer invoices.

- Apple Pay / Google Pay – These mobile wallet options are present but not yet top of mind for Italian consumers. Apple Pay in particular is offered by many Italian banks and supported at many online checkouts (our data saw Apple Pay on ~15,000 Italian sites, which is significant). Still, surveys suggest Apple Pay and Google Pay are among the least preferred methods in Italy (rapyd.net). Their significance lies in convenience for the subset of users who have them set up – they streamline card use on mobile. As more Italians use their phones for shopping, these methods might grow. For now, they act as nice-to-have options in B2C (and essentially not used in B2B).

- Local Banking and Cash Solutions – Italy has had some online banking payment attempts like MyBank (an EU-wide bank transfer system that was adopted by Italian banks) and the traditional bonifico (bank wire) for e-commerce. MyBank allows instant bank debits for online purchases, and some merchants do offer it. It hasn’t reached the ubiquity of Netherlands’ iDEAL, but it caters to those who prefer direct bank payment without cards. Cash on Delivery, while not a “payment provider,” is historically important in Italy – a portion of shoppers still choose to pay the courier in cash or card upon delivery. This method is declining year by year but remains in certain sectors (e.g. furniture, older demographics). Many merchants outsource the COD handling to logistics or just mark it as an option with a fee. It’s more relevant in B2C; B2B rarely uses COD (they’d just invoice).

- Stripe, Braintree and PSPs – International PSPs like Stripe are quite popular among Italian online businesses (Stripe is the second-most common integration after PayPal in our Italy data, found on ~19,000 sites). These platforms let merchants accept cards, wallets, and even local methods through one gateway. Braintree (owned by PayPal) similarly powers many Italian webshops behind the scenes, enabling both card processing and PayPal integration. Local acquirers like Nexi (CartaSi) and UniCredit’s solutions also have a big merchant base, especially for larger retailers. In effect, PSPs ensure that Italian merchants can accept the mix of payment forms consumers expect. They are crucial in both B2C and B2B (for example, a B2B software SaaS might use Stripe to bill Italian companies via credit card or Sofort, etc.). Some newer options like Revolut Pay have also entered Italy – indeed, our scan saw Revolut on ~14k sites (likely merchants adding the Revolut Pay button to cater to Revolut users). These are still niche but indicate a willingness of merchants to experiment beyond the traditional set.

Domestic vs International

Italian merchants historically catered to domestic buyers’ preferences (hence a heavy emphasis on PayPal). Now, with cross-border e-commerce growing (two-thirds of Italian shoppers have bought from international sites (rapyd.net)), Italian merchants are expanding their payment options. Many are adding methods like Amazon Pay (since Italians shop on Amazon’s platforms), or enabling multi-currency credit card processing to attract foreign customers. Likewise, foreign companies selling to Italy have learned that including PayPal at checkout is crucial – a UK or German site that adds PayPal might suddenly convert many more Italian buyers who trust PayPal over entering card details. We see platform-native solutions smoothing this process: for example, Shopify Payments allows a foreign merchant to offer Italian shoppers local payment options (like bonifico via Sofort or appropriate localized card forms) without that merchant needing an Italian banking relationship. Additionally, services like Klarna have recently launched in Italy as well, aiming to introduce more pay-later options; their usage is nascent but growing for cross-border purchases (e.g. an Italian buying from a German shop might use Klarna). In summary, Italy’s e-commerce shows a stark local preference for PayPal and familiar tools, and both domestic and international sellers adjust to that reality – often by prominently featuring PayPal, offering prepaid-friendly options, and maintaining trust signals. The reliance on platform solutions (PayPal, Amazon Pay, etc.) also lowers the friction of cross-border commerce for Italian consumers, effectively bridging domestic habits with international retail.

Norway: Vipps and Klarna

Norway’s consumers are highly digital and spend a lot online. Card payments are extremely common – in fact, Norway has one of the highest per-capita card usage rates. Cards (debit and credit combined) account for roughly 43% of all retail transactions (online and offline) in Norway (pay.com). The majority of these are through BankAxept, Norway’s domestic debit card system, which is co-branded with Visa/Mastercard for international acceptance (pay.com). Alongside cards, Norway has a very strong mobile payments culture thanks to Vipps, a mobile wallet app used by most Norwegians. Vipps has cornered the digital wallet market in Norway (pay.com), meaning alternatives like Apple Pay or Google Pay are secondary (though available). Klarna and other pay-later options are also popular – Norway, like other Nordics, embraced Klarna early for splitting or delaying payments. PayPal exists but plays a smaller role in day-to-day domestic payments (around 7% share of online transactions as per Norges Bank (pay.com)), used mainly for cross-border shopping. In summary, Norway’s landscape features high card usage with a layer of mobile wallet convenience and BNPL flexibility.

Key Providers and Roles:

- BankAxept (Card payments) – BankAxept is the domestic debit network, ensuring that payments using Norwegian bank cards are processed cheaply and efficiently inside Norway. Practically every Norwegian has a BankAxept card. Online, when a customer pays by “card,” it often routes through BankAxept if domestic, or via Visa/MasterCard rails if needed. For merchants, accepting cards is non-negotiable – it covers debit and credit usage. Credit card usage is growing in Norway (almost one credit card per person in circulation (pay.com), and many online purchases – especially higher value or travel bookings – go on credit cards. In B2B, cards can be used for convenience too, but many companies also use invoices. Nonetheless, cards form the backbone of Norwegian e-commerce payments, making up a large chunk of transactions by value.

- Vipps – Norway’s ubiquitous mobile payment app. Vipps allows users to pay online by confirming with their mobile number/app, similar to how one would use a wallet instead of entering card details. Virtually everyone in Norway knows and many use Vipps; it started as a peer-to-peer app but is now available for online checkouts, bill payments, etc. Vipps dominates Norwegian mobile payments, effectively sidelining other e-wallets domestically (pay.com). For online merchants, adding Vipps (via a PSP or Vipps API) can significantly smooth mobile conversion – a user can just choose Vipps and approve the purchase on their phone. Our data shows Vipps present on about 6,700 Norwegian sites, which implies a strong uptake (though not as high as MobilePay in DK, possibly because many international platforms were slower to integrate Vipps). In B2C, Vipps is extremely important, especially among younger shoppers and for quick purchases. In B2B, it’s less used (business purchases would more likely go via bank or invoice), but some small entrepreneurs might even accept Vipps for simplicity.

- Klarna – Norway is one of Klarna’s significant markets outside Sweden. Klarna’s BNPL and invoicing services are widely offered by Norwegian merchants. Notably, Klarna is reported to account for about 18% of domestic online retail sales in Norway (pay.com), which is substantial. Many Norwegian shoppers enjoy the option to “buy now, pay later” or split payments, and Klarna provides that with its usual smooth user experience. Norwegian merchants, especially in fashion, electronics, and other retail segments, integrate Klarna to boost sales and AOV (average order value). In our dataset, Klarna actually appeared as the top payment-related provider on Norwegian sites (~8,700 sites), even above PayPal, indicating how common it is. For B2C, Klarna is a key player. For B2B, Klarna has a business offering (Klarna for business/Tillit – a local BNPL startup mentioned) but these are less prevalent; businesses typically aren’t using Klarna to pay invoices. Still, the concept of paying after receiving goods is also present in B2B via invoices – just not via Klarna’s interface.

- PayPal – While not a leader domestically, PayPal has a steady presence in Norway. According to the central bank, it’s about 7% of online transaction volume (pay.com), which is modest, but it remains crucial for cross-border purchases. Norwegians shopping from international websites (where Vipps or Klarna might not be available) often rely on PayPal as a convenient and trusted method (pay.com). Likewise, Norwegian online sellers include PayPal to capture international sales or niche use cases. Our data found PayPal on ~8,300 Norwegian sites, nearly as many as Klarna. This suggests that even if Norwegians themselves don’t prioritize PayPal when domestic options exist, it’s still widely offered as a universal option. In B2B, PayPal usage would be rare except perhaps freelancers or software services.

- Other Methods/PSPs – Norway’s market sees involvement from Nordic PSPs like Nets (now part of Nexi, historically handled a lot of card processing), as well as Stripe (our data: ~6,000 sites, showing many Norwegian businesses use Stripe to accept cards and other methods). Swish (the Swedish mobile pay) is not used in Norway, but interestingly, MobilePay (from Denmark) was merged with Vipps – yet in our data MobilePay appears on ~3,600 Norwegian sites. This could indicate cross-border Danish merchants or some early adoption in Norway; however, post-merger Vipps will cover that. Another mention is “Klarna’s Kustom Checkout” (seen as “Kustom” on ~1,300 sites) – this appears to be a one-stop checkout solution possibly by Klarna to integrate multiple methods. It’s relatively small but shows innovation in unified checkout experiences. For B2B, beyond standard invoice, some specialized services like Aprila or Svea might offer trade financing, but they didn’t prominently show up in top 10. Vipps does have a business-facing product (Vipps Faktura) to send invoices via Vipps app – highlighting again how consumer tools in Norway often extend into business use.

Domestic vs International

Norway’s e-commerce players pay attention to both local preferences and the fact that Norway is outside the EU (which affects cross-border trade, VAT, etc.). Domestically, a Norwegian merchant will emphasize Vipps and Klarna alongside cards to maximize conversions – these are what local shoppers expect. Internationally, Norwegian merchants know that foreign customers won’t have Vipps, so they ensure card payments (Visa/Mastercard) and PayPal are available. Many also support Klarna’s global offering in other markets (since Klarna operates across Europe and even the US, a Norwegian merchant can offer pay-later to customers in those countries via Klarna). Moreover, with high English proficiency, Norwegians frequently shop abroad; when they do, they typically use cards or PayPal – indeed PayPal’s main utility in Norway is for cross-border purchases (pay.com). This behavior influences Norwegian e-commerce sites too: for example, the prevalence of PayPal on Norwegian sites is partly to reassure and facilitate sales to non-Norwegians (and to Norwegians who might prefer it in certain situations). Another interesting point is that as part of the Vipps-MobilePay merger, Nordic payment integration is improving – soon a Danish customer might pay a Norwegian shop with MobilePay and it seamlessly works with Vipps (and vice versa). This will strengthen cross-Nordic commerce by leveraging each country’s local wallet. In summary, Norway shows a pattern seen in the Nordics: very high local adoption of innovative payments, and a parallel support of global methods to engage in cross-border commerce.

Sweden: The land of Klarna and Swish

Sweden’s online payment landscape has two giants: Klarna and Swish. It’s often said that “everyone in Sweden uses Swish,” and that’s barely an exaggeration – about 98% of Swedish adults have Swish installed and ~95% use it regularly (ergomania.eu). Swish is a mobile payment system (bank account-linked) originally for P2P but now widely used in e-commerce and even brick-and-mortar. On the other hand, Klarna’s pay-later services (invoice, installment, etc.) account for a huge portion of Swedish e-commerce – over 50% of online transactions by value are open invoice payments (adyen.com) - many of those facilitated by Klarna and a handful of competitors. Credit/debit cards remain popular too (especially for some online services and travel), but Sweden stands out in that invoices/payment after delivery are the single largest category, surpassing cards (adyen.com). This is rooted in consumer behavior: Swedes historically liked to receive goods and pay by invoice, a practice that fintechs like Klarna turned into a smooth digital experience. Meanwhile, Swish’s instant bank transfers are siphoning off transactions that might have been card or cash. PayPal exists and is used in Sweden, but given the strong local options, it’s not a leading method for domestic shopping. Overall, Sweden is extremely advanced: high smartphone usage, multiple fintech solutions, and consumers comfortable with alternative payments.

Key Providers and Roles:

- Klarna – The poster child of Swedish fintech, Klarna is omnipresent in Swedish e-commerce. It started with “Få först, betala sen” (get first, pay later) invoice payments and now offers everything from 30-day invoicing to installment plans and a smooth one-click checkout (Klarna Checkout) that many Swedish sites use as their entire payment frontend. Klarna claims a large share of the market – indeed open invoice methods (dominated by Klarna) exceed half of ecom transactions (adyen.com). In our data, Klarna was on ~22,300 Swedish sites, more than any other provider, which underlines its reach. For consumers, Klarna’s appeal is the flexibility and trust (you can return items before paying, etc.). For merchants, offering Klarna can increase sales, but it comes with fees – still, in Sweden it’s expected. Klarna also now includes card payments and even bank direct payments in its checkout, so some merchants use Klarna Checkout as a one-stop solution (which might also explain why cards are less separately visible). In B2C, Klarna is king. In B2B, while Klarna has business solutions, Swedish companies often rely on traditional invoicing (sometimes using competitors like Svea or just direct billing) for trade credit. Klarna’s brand is primarily consumer-focused in Sweden.

- Swish – A mobile payment app backed by Sweden’s banks. Swish lets users instantly transfer money using just a phone number. It’s extremely popular for splitting bills, paying small merchants, and increasingly, paying online. Now, Swish is the most frequently used payment service in Swedish online shops and apps (snb.ch) by number of transactions. By 2024, more Swedes named Swish as their leading online payment brand over Klarna, which it overtook in popularity a few years ago (statista.com). For e-commerce, merchants display a Swish option; if chosen, the shopper approves the payment in the Swish app (which debits their bank). It’s effectively like a real-time bank transfer with mobile convenience. Swish is used for both B2C and informal B2B (e.g. small business or sole trader payments). For larger B2B, not so much, as companies prefer invoicing and not all have Swish for business set up. But Swish does have a business product and even charities, clubs etc. use Swish for payments. With 8+ million users (in a country of 10 million (ergomania.eu), any e-commerce catering to Sweden almost needs to accept Swish now.

- Cards (Visa/Mastercard) – Despite the dominance of Klarna and Swish, cards still account for a significant chunk (around one-third of Swedish online payments by some estimates (ppro.com). Many Swedes have credit cards (often incentivized by loyalty programs) and still use them especially on sites that don’t offer Klarna or Swish (or for services like subscriptions, streaming, etc.). Swedish-issued cards are often co-badged with BankAxept-like debit or just are international Visas/Mastercards. Merchants usually accept cards via PSPs or via Klarna’s infrastructure. The interesting dynamic is that because Klarna Checkout can handle card payments, a shopper might enter card details on a Klarna form – from the user perspective they might not even realize the payment is by traditional card because Klarna or Swish overshadow it. In B2B, corporate cards might be used for things like travel bookings or online services (Swedish businesses have high card adoption for expenses). So cards remain an important method for both consumers and businesses, even if less celebrated.

- Svea, Walley, and other BNPL/Invoice providers – Sweden has several other players in the invoice/payment plan space: Svea Ekonomi, Walley (Collector), Avarda, AfterPay (Riverty), etc. Adyen’s guide noted 5–6 providers offering invoices in Sweden (adyen.com). Klarna is the largest, but these others carve out niches (for example, Svea might power payments for some smaller retailers or specific sectors). Our data saw Svea on ~2,980 Swedish sites – notable though much smaller than Klarna’s footprint. These services often target both B2C and B2B (Svea and Walley have business credit solutions). For a merchant, choosing one of these can be about better fees or industry-specific offerings. The proliferation of invoice providers underscores how ingrained buy-now-pay-later is in Swedish commerce – there’s competition to grant consumers that convenience of paying after delivery.

- PayPal and global wallets – PayPal is available in Sweden and quite a few Swedes have accounts, but its usage is limited compared to local solutions. It tends to be used for cross-border transactions (e.g. buying on international sites) or on marketplaces. Many Swedish merchants still offer PayPal – our data found it on ~18,600 sites – often as a “why not” addition for the few customers who prefer it or for foreign customers. Apple Pay and Google Pay are also supported by Swedish banks/cards and sometimes listed on checkouts (Apple Pay was on ~9,100 Swedish sites per our data). They haven’t achieved the same usage as Swish, but they do provide a fast checkout option especially for mobile and for users with international backgrounds. They’re more of a complement; for instance, a tech-savvy shopper might use Apple Pay on an iPhone instead of Swish if they find it quicker.

Domestic vs International: Swedish e-commerce players are very outward-looking (Swedes buy from international sites and Swedish sites sell abroad, especially to the EU). For domestic sales, not offering Klarna or Swish is almost unthinkable for a mainstream merchant – you’d lose too many sales. For cross-border, Swedish merchants rely on those platform capabilities: Klarna is expanding in many markets, so a Swedish merchant can offer Klarna in, say, Germany or the UK to attract foreign customers similarly. Swish, however, is domestic; a non-Swedish customer cannot use Swish, so Swedish merchants must also have card payments and PayPal to cover foreigners. This they generally do – either via a PSP or via Klarna Checkout (which by default shows local Swedish options but can fall back to card for others). International merchants entering Sweden often partner with Klarna to quickly gain local credibility. It’s common for foreign brands launching Swedish sites to heavily feature Klarna and Swish logos – it signals to Swedish shoppers that “you can trust and pay easily here”. Additionally, Sweden’s high trust in fintech means new entrants can get traction – e.g. Stripe is used by many startups in Sweden and can process Swish via plugins, so newcomers can offer Swish with minimal effort. Platform-native solutions like Shopify Payments also support local methods in Sweden (Shopify merchants can enable Klarna and Swish through integrations), which lowers the barrier for smaller foreign merchants to sell to Swedes. A noteworthy cross-border trend is the Nordics integration: with Vipps, MobilePay, and Swish collaborating, a merchant in one Nordic country might soon accept a wallet payment from a neighboring country’s app seamlessly. This will further blur domestic vs international in the Nordic region’s payments. All told, Sweden’s market is characterized by extremely strong local preferences (Swish, invoicing) that any successful player must adapt to, and a parallel accommodation of global methods for complete coverage. Swedish consumers will happily use a local method if available, but if shopping on a foreign site, they might use a card or PayPal – however, their expectation now is that more and more foreign sites will cater to them with Swedish methods.

Platform-native integrations and cross-market presence

One recurring theme across all these countries is the role of platform-native payment integrations – especially on popular e-commerce platforms like Shopify and WooCommerce – in streamlining cross-border payment acceptance. Two prime examples are Shopify Payments (with its local method support) and PayPal’s ubiquitous plugins.

Shopify Payments (and Shop Pay)

Shopify Payments is the built-in payment gateway for Shopify merchants, powered behind the scenes by providers like Stripe/Adyen. Crucially, it automatically enables relevant local payment methods based on the shopper’s region. For instance, a Shopify merchant in the US can easily accept Bancontact and iDEAL when selling to Belgium or the Netherlands – they simply toggle those on, no custom integration needed (help.shopify.com). Shopify Payments supports Bancontact, iDEAL, Sofort, EPS, Klarna, etc., depending on the market (help.shopify.com), meaning merchants on Shopify can localize their checkout experience at the flick of a switch. This has huge implications: it lowers the barrier for cross-market expansion since even small merchants can offer country-specific popular methods without in-depth knowledge. Additionally, Shop Pay, Shopify’s accelerated checkout, is available globally – it stores customer details for one-click payments across any Shopify store. Shop Pay itself isn’t a separate payment method funded by a bank or card, but it streamlines card payments and now even installments (Shop Pay Installments by Affirm in some countries). Its presence (noted in our data across countries, e.g. ~6–13k sites in each country had “Shop Pay” enabled) underscores the impact of platform features. Shop Pay improves conversion and thus indirectly encourages merchants to sell globally, knowing returning customers can pay faster. In essence, platform-native solutions like Shopify Payments abstract away complexity: a single integration gives a merchant Apple Pay, Google Pay, local methods and credit cards in one – very powerful for cross-border commerce.

WooCommerce & PayPal/Stripe integrations

WooCommerce (the popular WordPress e-commerce plugin) relies on third-party payment gateways. PayPal and Stripe are two that have become nearly universal on WooCommerce sites globally. Because they are easy to install and free to use (no monthly fee, just transaction fees), many WooCommerce-based shops simply offer PayPal and Stripe out-of-the-box. This means an English WooCommerce site, a German one, or a Danish one – all likely have a similar PayPal checkout option (and Stripe powering card payments). Our analysis of PayPal’s presence found that a significant percentage of Shopify and WooCommerce stores across these countries have PayPal enabled – often 50% or more (e.g. ~72% in Italy, ~47% in Sweden, ~40% in Finland, ~62% in Belgium) based on the data of PayPal usage on those platform stores. This prevalence is no accident: PayPal comes built-in with Shopify and as a default plugin with WooCommerce, so many merchants leave it on as a convenient global method. The result is a kind of cross-market ubiquity – no matter if you’re shopping on a boutique in Oslo or a gadget store in Milan, you’re likely to see the PayPal button. That consistency gives consumers a familiar fallback and gives merchants confidence they can serve international customers (who might prefer PayPal if they’re unfamiliar with the local method on that site). Stripe’s integration on WooCommerce similarly allows merchants worldwide to accept not just cards but Apple Pay, Google Pay, and even local methods (if configured) like iDEAL or Klarna through Stripe. So, platform ecosystems have made a set of payment methods effectively universal across markets.

Cross-Border Influence of Key Players

Certain providers emerge as bridges across countries. PayPal is the obvious one – present virtually everywhere, it’s the default cross-border wallet. Stripe/Adyen as PSPs power many local methods but are invisible to consumers; their influence is in enabling merchants to support the right mix in each market. Klarna has grown from a Swedish BNPL to a global brand now active in all the discussed countries – a German shopper, a Norwegian, an Italian can all use Klarna, making it a cross-border payment option in its own right. Apple Pay and Google Pay – while not top of any country’s list except perhaps on tech-centric sites – provide a unified experience for a segment of users across borders (a tech-savvy Swiss or Italian might choose Apple Pay in lieu of typing card details, for example). Mollie and Nets/Nexi (regional PSPs) are extending beyond their home (Mollie from NL into Belgium, France, etc., Nets from Nordics into DACH), contributing to cross-pollination of methods.

In summary, platform-native integrations and globally-oriented providers smooth out the differences between markets. They ensure that a merchant doesn’t have to integrate Bancontact, iDEAL, Klarna, Swish separately with different contracts – instead, one integration (be it Shopify Payments, PayPal, Stripe, etc.) covers it. This has led to a situation where key payment methods achieve strong cross-border presence despite being local in nature: for example, Bancontact can be accepted by a German Shopify store selling to Belgium, and iDEAL appears on UK websites via PayPal’s Braintree or Adyen. Likewise, a Dutch merchant can easily offer Klarna to German customers through a single PSP. The significance is huge for market entry and expansion: a merchant can enter a new European market and immediately offer the familiar local payment options through their existing platform, rather than needing to sign deals with local banks. This greatly lowers friction in European e-commerce, effectively enabling the regional patterns we’ve discussed to coexist with global e-commerce flows.

Conclusion: Regional patterns, cross-border champions, and the power of local preferences

Analysing these seven countries side by side reveals clear regional patterns and instructive differences:

Local dominance vs global universals

Each country has one or two dominant local payment methods – Bancontact in Belgium, Twint in Switzerland, MobilePay in Denmark, Paytrail (bank transfers) in Finland, PayPal (local favourite) in Italy, Vipps (and cards) in Norway, Klarna/Swish in Sweden. These methods stem from local banking systems or consumer habits and command loyalty in their home markets. At the same time, global methods like credit cards and PayPal are present “just about everywhere” (retaildetail.eu) as the common denominators. Cards are accepted in all countries (even if not always first choice), and PayPal’s familiar checkout is offered broadly to capture cross-border shoppers. This duality means successful merchants typically combine the local must-haves with a baseline of global options.

North vs south vs central

There’s a north-south divide of sorts. The Nordics (Denmark, Norway, Sweden, Finland) are heavy on mobile wallets and pay-later solutions: MobilePay/Vipps/Swish and Klarna/Svea are household names there, reflecting a tech-forward consumer base and trust in digital finance. Central-West Europe (Belgium, Netherlands, Switzerland) leans on bank-based payments: Bancontact, iDEAL, Twint, Sofort – these are all bank-account-direct methods, indicating the strength of bank networks and a preference for direct debit-style payments. Southern Europe (Italy) has been more cautious historically, thus PayPal (a “foreign” but trust-building method) and cash/prepaid solutions took hold. Understanding these cultural and historical contexts is key – one size does not fit all in Europe. A Nordics-focused merchant will prioritise mobile wallets and Klarna, whereas a Benelux-focused one must integrate local bank payments or risk losing most customers.

Cross-border influencers – key players

Some payment providers have clearly managed to extend their influence across multiple countries: Klarna (originating in Sweden) is now a major player in Norway, Finland, the Netherlands, Belgium, etc., showing that a popular concept can travel – especially BNPL in regions with similar consumer credit cultures. PayPal remains a pan-European staple for cross-border commerce – even where it’s not #1 locally, it’s the safety net for transactions that cross languages or currencies. Stripe and Adyen (though behind the scenes) power a lot of this by enabling local method acceptance to non-local merchants – they are the unsung heroes making, for example, a French website feel native to a Dutch customer by offering iDEAL. Mollie has grown beyond the Netherlands into Belgium and even across Europe, thanks to its easy integration – it’s becoming a regional champion for SME payments. Meanwhile, regional collaborations (like the Vipps-MobilePay merger and its partnership with Swish) hint at the future: key local methods might interoperate across borders, effectively becoming multi-country methods. If that succeeds, a Nordic wallet could rival card schemes in cross-border utility within that region.

Platform power – shaping market entry

The prevalence of Shopify, WooCommerce, Magento, and other platforms in online retail has greatly shaped how payments are adopted. These platforms have baked-in support for the dominant providers, which means merchants expanding to a new country often have the tools at their fingertips to accept the local payments. For example, a Canadian brand using Shopify entering the Dutch market can enable iDEAL and Bancontact via Shopify Payments in minutes – something that would have been a project on its own a decade ago. This reduces the friction of market expansion; payment localization is no longer a barrier reserved for enterprise retailers with local contracts, but available to SMBs. It also means that certain payment methods achieve widespread adoption simply by being defaults on platforms – PayPal’s presence on WooCommerce is a clear case. In effect, the e-commerce platforms act as conduits for spreading payment innovations across borders. If tomorrow a new payment method becomes huge in one country, chances are platform providers or PSPs will integrate it and thereby propagate it across thousands of merchants in multiple countries (much like Apple Pay rolled out or Klarna became a checkout option globally).

Consumer behaviour and trust

Underpinning all of this, local consumer behaviour and trust patterns dictate what gets used. In Belgium and Netherlands, trust in one’s bank and domestic systems is high – hence bank-based methods flourish. In Italy, wariness about fraud led to a trust in PayPal and cash – only now gradually shifting toward more modern solutions as trust improves. Nordics have high trust both in technology and in credit, enabling things like Swish and Klarna to thrive. These patterns highlight that any payment provider trying to enter a new European market must contend with deeply ingrained habits. Often, partnering or integrating with existing local systems (as Mastercard did by co-badging Bancontact, or as Klarna did by offering localised invoice terms) is more successful than trying to impose a wholly new behaviour.

To conclude, European e-commerce payments are a mix of local traditions and global tech. Merchants aiming for success across these markets need to literally “speak the language” of payments in each country – be it offering installment invoices in Sweden, MobilePay in Denmark, or Bancontact in Belgium – while also providing cross-border staples like cards and PayPal to ensure no customer is left out. The good news is that modern payment platforms and providers have made this mapping far easier. The direction is clear: meet customers’ local expectations at checkout, and they will buy confidently, whether they’re next door or across the continent. By recognizing the strengths and focus of each payment provider (from Twint’s local sovereignty in Switzerland to PayPal’s cross-border indispensability), businesses can craft a payment strategy that feels native in every market they serve, B2C and B2B alike. This localized approach, backed by data and smart integrations, is increasingly what defines competitive advantage in Europe’s vibrant online payments landscape.

More from

Market Intelligence

category

Spain counts 89,038 active online retailers, with clothes & shoes leading the category mix, an estimated +1,2bn parcels/year, and average delivery prices at €4,9 (home) vs €4,4 (OOH) for lightweight items. Our new Spain report maps the market structure, checkout dynamics, delivery methods, and how the main carriers compete for visibility - including the often-overlooked impact of white-label checkouts.

If you’re working in last-mile delivery and want a competitive view of Spain, download the full report here.

Spanish last-mile delivery market analysis

This report focuses on nine of the largest delivery providers in Spain: Correos / Correos Express, MRW, GLS, SEUR/DPD/Tipsa, DHL, NACEX, FedEx/TNT, CTT, and InPost/Mondial Relay. End-to-end retail & logistics operators (e.g., Amazon) and smaller/specialised operators (refrigerated, oversized, etc.) are intentionally excluded to keep the comparison clean and actionable.

All figures are based on Tembi’s continuous monitoring and analysis of Spanish online retailers and checkout setups, with consistent classification to support like-for-like analysis across markets. Use it to maintain competitive advantage, capture share in attractive segments, and understand market dynamics with clarity.

Quick takeaways

- Market scale: 89,038 active online retailers; +1,2bn parcels/year; e-commerce CAGR (2019–2024) estimated at ~14,3%.

- White-label: A majority of retailers hide carrier brands in checkout (white-label) - a major visibility opportunity for carriers.

- Competitive landscape: Correos / Correos Express leads by share of presence and also wins the first checkout position most often; GLS and SEUR/DPD/Tipsa follow.

- Delivery prices: Average lightweight delivery prices sit around €4,9 home vs €4,4 OOH, with OOH still underpenetrated.

Market overview: size, growth & drivers

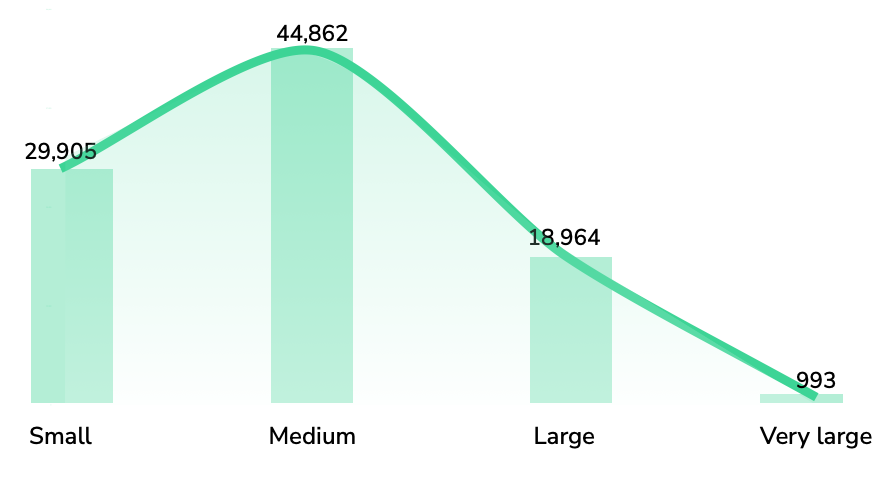

Spain is home to nearly 90,000 active online retailers, with a long tail that still produces meaningful parcel demand - and a smaller set of large/very large retailers that set service expectations (speed, returns, OOH availability, and delivery choice). Category-wise, Spain’s retailer base is led by clothes and shoes (~12,19%), followed by health & medicine (~7,04%) and beauty & personal care (~6,3%).

Delivery provider landscape: who dominates?

In Spain, share of presence (where a provider appears as an option in checkout) is heavily led by Correos / Correos Express, which shows up across ~41% of branded checkouts in our dataset, far ahead of the next tier (MRW, GLS, SEUR/DPD/Tipsa).

But presence is only half the story. In checkout, position matters.

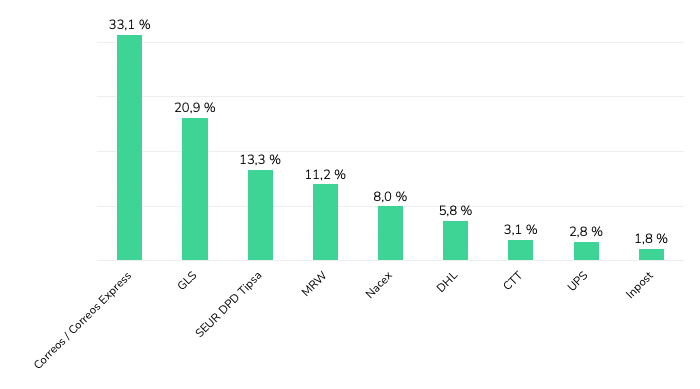

Across Spanish webshops where delivery provider brands are visible, Correos / Correos Express holds the first position most frequently (33,1%), followed by GLS (20,9%) and SEUR / DPD / Tipsa (13,3%). MRW (11,2%) and NACEX (8,0%) follow, with DHL (5,8%) and smaller shares for others.

If you read our Italy last-mile delivery analysis, you’ll recognise the same core idea: the checkout is the battlefield. The winners aren’t only those with the biggest networks - they’re the providers most consistently prioritised where consumers actually make the choice - why checkout position and visibility are a key differentiators in revenue and brand building.

White-label checkouts: the hidden market

Here is the uncomfortable truth for last-mile brands: a large share of Spanish retailers don’t show carrier names at all - they show only delivery methods and prices.

- In the broader dataset view, over 62% of retailers run delivery options in a way that hides carrier brands.

- In the size-categorised subset (76,615 retailers), 58% use white-label checkout, and the share varies by retailer size.

This matters because it means “market share” can look very different depending on whether you measure parcel volumes, merchant relationships, or brand visibility to consumers. For carriers, improving brand exposure inside white-label environments is one of the largest untapped levers in Spain - because it’s not a network problem, it’s a checkout/integration problem.

Delivery methods: home still dominates, OOH is growing

Across the market, home delivery is still the default, and the regulator view aligns with what we see in retailer setups: CNMC reports that in 2024 the usual delivery place was home (68,9%), with PUDO/convenience points (13,6%) and lockers (3,8%).

When we look at delivery methods displayed across retailers (excluding white-label checkouts), the same story holds: OOH is present, but underbuilt - especially compared to where Spain could go given consumer density and the cost-to-serve logic that OOH enables.

And pricing reinforces the direction of travel: for lightweight items, average delivery prices are roughly €4,9 (home) vs €4,3–€4,5 (OOH) depending on parcel shop vs locker. Spain is also cheaper than Italy across all options, which changes the “room” carriers have to subsidise adoption - but not the underlying incentive to densify OOH.

Pricing patterns by method and provider

While retailers set the price shown in checkout, these figures consistently reflect provider positioning.

- Home delivery is generally the most expensive method.

- DHL sits at the upper end (consistent with express and international positioning).

- GLS, SEUR/DPD, and NACEX cluster around the market average.

- Correos is typically offered as one of the cheaper options.

Provider portfolios: size mix, category mix, and growth potential

Not all “presence” is equal. The value of a provider’s retailer base depends on who those retailers are.

Using Tembi’s size scoring (0–100), we can see clear portfolio skews:

- InPost and DHL have the highest average webshop size scores (both ~high-50s), meaning their client bases lean larger.

- CTT also skews larger.

- MRW is most weighted towards smaller retailers.

- Correos, SEUR/DPD/Tipsa, GLS, and NACEX sit closer to the market middle.

Category exposure shows the same idea from a different angle: providers aren’t just “generalists” - each ends up with a distinct category footprint (e.g., stronger concentration in health & medicine, fashion, electronics, etc.)

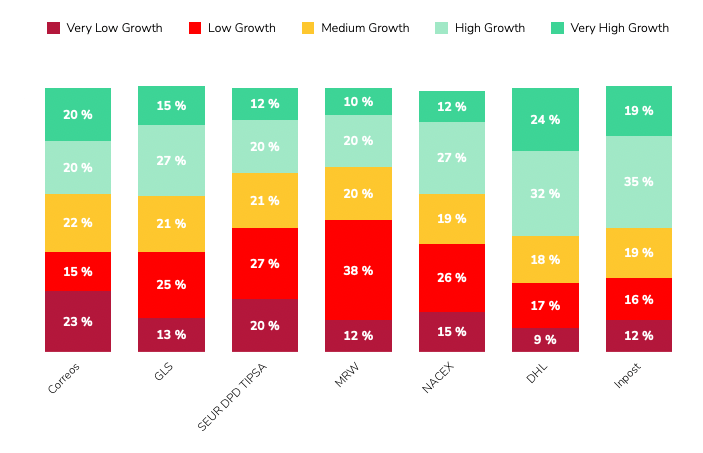

Finally, our Growth Indicator model adds a forward-looking layer: DHL and InPost have the strongest growth-weighted portfolios, with 56% and 54% of their clients forecast to be in high or very high growth bands. Correos shows a more balanced mix across growth bands.

Strategic implications for market planning

If you want the practical “so what” for Spain, three things stand out:

- Treat white-label checkout as a growth surface

With most retailers hiding carrier brands, increasing visibility isn’t just marketing - it’s product, partnerships, and integration strategy. - OOH is still early, and it will reshape the economics

Spain’s home-dominant delivery mix is not a fixed state. As locker and parcel shop networks densify, both carrier cost-to-serve and retailer checkout strategy will shift. - Benchmark portfolios, not just presence

Provider footprints differ by retailer size, category exposure, and growth outlook. If you’re not tracking that mix, you’ll misread where your future parcel volume will come from.

Conclusion

Spain’s last-mile market is large, competitive, and still structurally under-optimised in checkout. Correos dominates branded presence and first-position frequency, white-label checkouts hide a big part of the market, and OOH remains a clear runway - with meaningful differences in portfolio quality and growth potential across providers.

Download the full Spain report, or schedule a Tembi demo to see your competitive landscape updated continuously across markets - including comparisons to our Italy analysis

Spain counts 89,038 active online retailers, with clothes & shoes leading the category mix, an estimated +1,2bn parcels/year, and average delivery prices at €4,9 (home) vs €4,4 (OOH) for lightweight items. Our new Spain report maps the market structure, checkout dynamics, delivery methods, and how the main carriers compete for visibility - including the often-overlooked impact of white-label checkouts.

If you’re working in last-mile delivery and want a competitive view of Spain, download the full report here.

Spanish last-mile delivery market analysis

This report focuses on nine of the largest delivery providers in Spain: Correos / Correos Express, MRW, GLS, SEUR/DPD/Tipsa, DHL, NACEX, FedEx/TNT, CTT, and InPost/Mondial Relay. End-to-end retail & logistics operators (e.g., Amazon) and smaller/specialised operators (refrigerated, oversized, etc.) are intentionally excluded to keep the comparison clean and actionable.

All figures are based on Tembi’s continuous monitoring and analysis of Spanish online retailers and checkout setups, with consistent classification to support like-for-like analysis across markets. Use it to maintain competitive advantage, capture share in attractive segments, and understand market dynamics with clarity.

Quick takeaways

- Market scale: 89,038 active online retailers; +1,2bn parcels/year; e-commerce CAGR (2019–2024) estimated at ~14,3%.

- White-label: A majority of retailers hide carrier brands in checkout (white-label) - a major visibility opportunity for carriers.

- Competitive landscape: Correos / Correos Express leads by share of presence and also wins the first checkout position most often; GLS and SEUR/DPD/Tipsa follow.

- Delivery prices: Average lightweight delivery prices sit around €4,9 home vs €4,4 OOH, with OOH still underpenetrated.

Market overview: size, growth & drivers

Spain is home to nearly 90,000 active online retailers, with a long tail that still produces meaningful parcel demand - and a smaller set of large/very large retailers that set service expectations (speed, returns, OOH availability, and delivery choice). Category-wise, Spain’s retailer base is led by clothes and shoes (~12,19%), followed by health & medicine (~7,04%) and beauty & personal care (~6,3%).

Delivery provider landscape: who dominates?

In Spain, share of presence (where a provider appears as an option in checkout) is heavily led by Correos / Correos Express, which shows up across ~41% of branded checkouts in our dataset, far ahead of the next tier (MRW, GLS, SEUR/DPD/Tipsa).

But presence is only half the story. In checkout, position matters.

Across Spanish webshops where delivery provider brands are visible, Correos / Correos Express holds the first position most frequently (33,1%), followed by GLS (20,9%) and SEUR / DPD / Tipsa (13,3%). MRW (11,2%) and NACEX (8,0%) follow, with DHL (5,8%) and smaller shares for others.

If you read our Italy last-mile delivery analysis, you’ll recognise the same core idea: the checkout is the battlefield. The winners aren’t only those with the biggest networks - they’re the providers most consistently prioritised where consumers actually make the choice - why checkout position and visibility are a key differentiators in revenue and brand building.

White-label checkouts: the hidden market

Here is the uncomfortable truth for last-mile brands: a large share of Spanish retailers don’t show carrier names at all - they show only delivery methods and prices.

- In the broader dataset view, over 62% of retailers run delivery options in a way that hides carrier brands.

- In the size-categorised subset (76,615 retailers), 58% use white-label checkout, and the share varies by retailer size.

This matters because it means “market share” can look very different depending on whether you measure parcel volumes, merchant relationships, or brand visibility to consumers. For carriers, improving brand exposure inside white-label environments is one of the largest untapped levers in Spain - because it’s not a network problem, it’s a checkout/integration problem.

Delivery methods: home still dominates, OOH is growing

Across the market, home delivery is still the default, and the regulator view aligns with what we see in retailer setups: CNMC reports that in 2024 the usual delivery place was home (68,9%), with PUDO/convenience points (13,6%) and lockers (3,8%).

When we look at delivery methods displayed across retailers (excluding white-label checkouts), the same story holds: OOH is present, but underbuilt - especially compared to where Spain could go given consumer density and the cost-to-serve logic that OOH enables.

And pricing reinforces the direction of travel: for lightweight items, average delivery prices are roughly €4,9 (home) vs €4,3–€4,5 (OOH) depending on parcel shop vs locker. Spain is also cheaper than Italy across all options, which changes the “room” carriers have to subsidise adoption - but not the underlying incentive to densify OOH.

Pricing patterns by method and provider

While retailers set the price shown in checkout, these figures consistently reflect provider positioning.

- Home delivery is generally the most expensive method.

- DHL sits at the upper end (consistent with express and international positioning).

- GLS, SEUR/DPD, and NACEX cluster around the market average.

- Correos is typically offered as one of the cheaper options.

Provider portfolios: size mix, category mix, and growth potential

Not all “presence” is equal. The value of a provider’s retailer base depends on who those retailers are.

Using Tembi’s size scoring (0–100), we can see clear portfolio skews:

- InPost and DHL have the highest average webshop size scores (both ~high-50s), meaning their client bases lean larger.

- CTT also skews larger.

- MRW is most weighted towards smaller retailers.

- Correos, SEUR/DPD/Tipsa, GLS, and NACEX sit closer to the market middle.

Category exposure shows the same idea from a different angle: providers aren’t just “generalists” - each ends up with a distinct category footprint (e.g., stronger concentration in health & medicine, fashion, electronics, etc.)

Finally, our Growth Indicator model adds a forward-looking layer: DHL and InPost have the strongest growth-weighted portfolios, with 56% and 54% of their clients forecast to be in high or very high growth bands. Correos shows a more balanced mix across growth bands.

Strategic implications for market planning

If you want the practical “so what” for Spain, three things stand out:

- Treat white-label checkout as a growth surface

With most retailers hiding carrier brands, increasing visibility isn’t just marketing - it’s product, partnerships, and integration strategy. - OOH is still early, and it will reshape the economics

Spain’s home-dominant delivery mix is not a fixed state. As locker and parcel shop networks densify, both carrier cost-to-serve and retailer checkout strategy will shift. - Benchmark portfolios, not just presence

Provider footprints differ by retailer size, category exposure, and growth outlook. If you’re not tracking that mix, you’ll misread where your future parcel volume will come from.

Conclusion

Spain’s last-mile market is large, competitive, and still structurally under-optimised in checkout. Correos dominates branded presence and first-position frequency, white-label checkouts hide a big part of the market, and OOH remains a clear runway - with meaningful differences in portfolio quality and growth potential across providers.

Download the full Spain report, or schedule a Tembi demo to see your competitive landscape updated continuously across markets - including comparisons to our Italy analysis

Italy counts 94,724 online retailers, with clothing, groceries and beauty leading the mix, average home delivery cost at €6.5 and OOH at €5.8. With continued investment and InPost’s strong market entry, OOH delivery is expanding rapidly and reshaping the competitive landscape. This Italian last-mile delivery market analysis maps the structure, methods and provider portfolios behind the numbers.

Working in last-mile delivery and interested in another competitive market analysis beyond Italy? Let's connect. Download the full report here.

Italian last-mile delivery market analysis

Italy remains one of Europe’s most active e-commerce markets by merchant count and parcel flow. To help last-mile executives benchmark strategy, this report profiles the market composition, delivery method availability and pricing, and the competitive landscape across six core providers: GLS, Poste Italiane, DPD BRT, DHL, InPost, and FedEx (TNT). You’ll see where demand concentrates by category, how pricing positions each method, and how provider client portfolios skew by retailer size and expected growth.

All figures are derived from Tembi’s continuous monitoring and analysis of Italian online retailers and checkout setups, with consistent taxonomy and normalisation to support like-for-like comparisons. Use it to maintain competitive advantage, capture share in attractive segments, and understand market dynamics with clarity.

Quick takeaways

- Market scale: 94,724 active online retailers with an expected CAGR of 4,5%.

- Method economics: Average home delivery (non-express) €6.5 vs OOH €5.8; OOH grows, but still underrepresnted.

- Competitive mix: GLS and Poste Italiane show the broadest share of presence; first-position frequency is led by GLS, followed by DPD BRT and Poste Italiane.

- White-label checkout: over 50% of retailers don't provide delivery choice by brand, just method.

Market overview: size, growth & drivers

Italy’s 94,724-strong retailer base skews to clothes & shoes (≈12.1%), then food & groceries (≈6.7%), and beauty (≈5.4%). The size pyramid shows most merchants are medium, fewer large, and about 1% very large, indicating a wide long-tail with concentrated head accounts that influence parcel mix and service expectations. The latest available data from 2020 suggest that around 830 million parcels are shipped domestically each year. Given the latest e-commerce growth estimation of an average annual growth rate of 4.5%, parcel volumes could now be approaching one billion shipments.

Delivery provider landscape: who dominates?

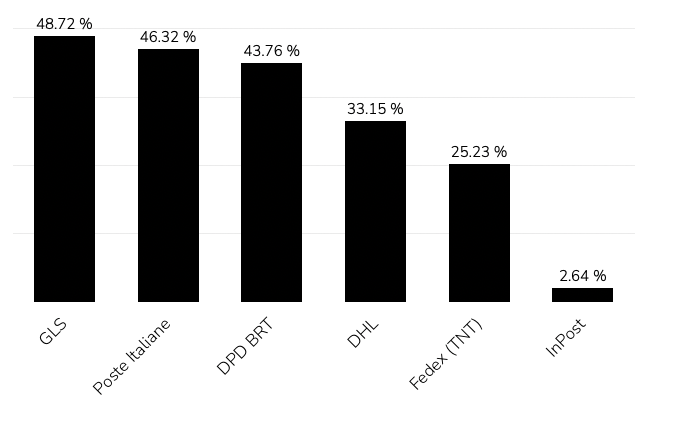

GLS and Poste Italiane hold the broadest presence across Italian webshops - GLS appears in 48.7% of retailer checkouts and Poste Italiane in 46.3%. DPD BRT, DHL, InPost, and FedEx (TNT) follow, forming the rest of the competitive landscape.

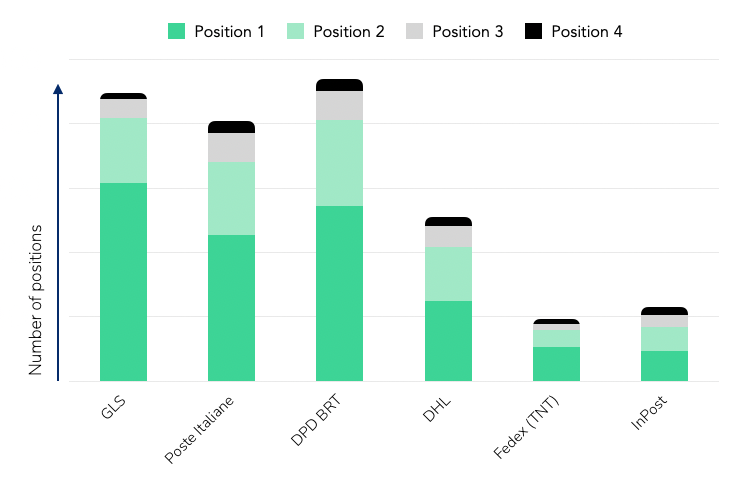

When looking at the first delivery option offered to shoppers, GLS leads with roughly 30%, followed by DPD BRT (26%) and Poste Italiane (22%).This ordering pattern reflects how retailers prioritise providers based on network reach, reliability, and negotiated terms rather than pure visibility.

In short:

- GLS commands the widest network and often the top checkout position.

- Poste Italiane mirrors that reach with strong national coverage.

- DPD BRT competes closely in second- and third-position slots, supported by regional partnerships.

- InPost and DHL show smaller overall shares but specialise in lockers and express shipments respectively.

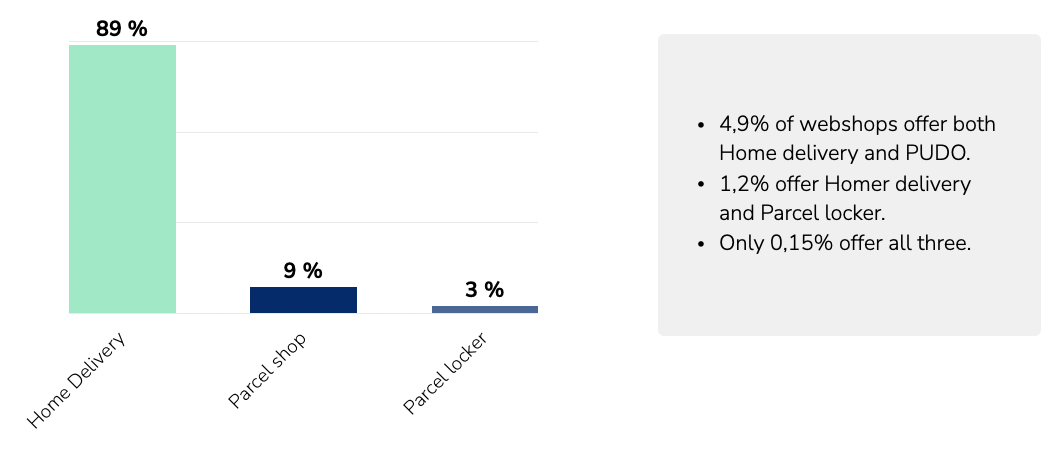

Delivery methods: consumer options and OOH uptake

Across Italian retailers, home delivery remains dominant, offered by roughly 89% of webshops. Parcel shops (≈9%) and parcel lockers (≈3%) are still at an early stage of rollout, but both formats are expanding as networks and integrations mature.

The limited share of OOH options reflects the market’s current infrastructure capacity rather than consumer demand alone. With continued investment from providers such as InPost, Poste Italiane, and DPD BRT, OOH coverage is expected to increase steadily over the next few years, giving retailers broader flexibility in how they structure delivery choices and costs.

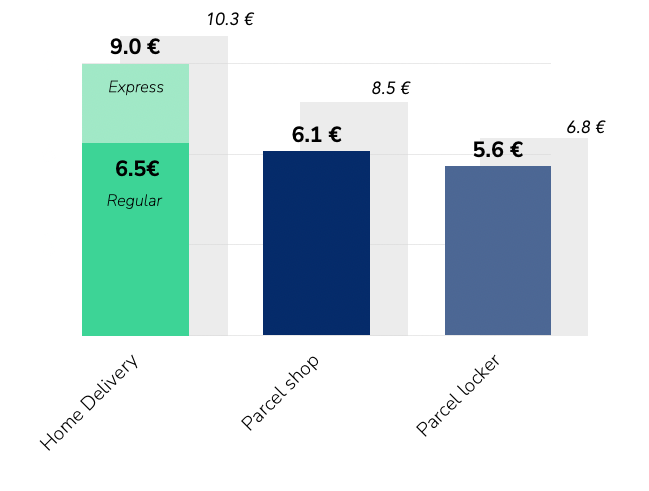

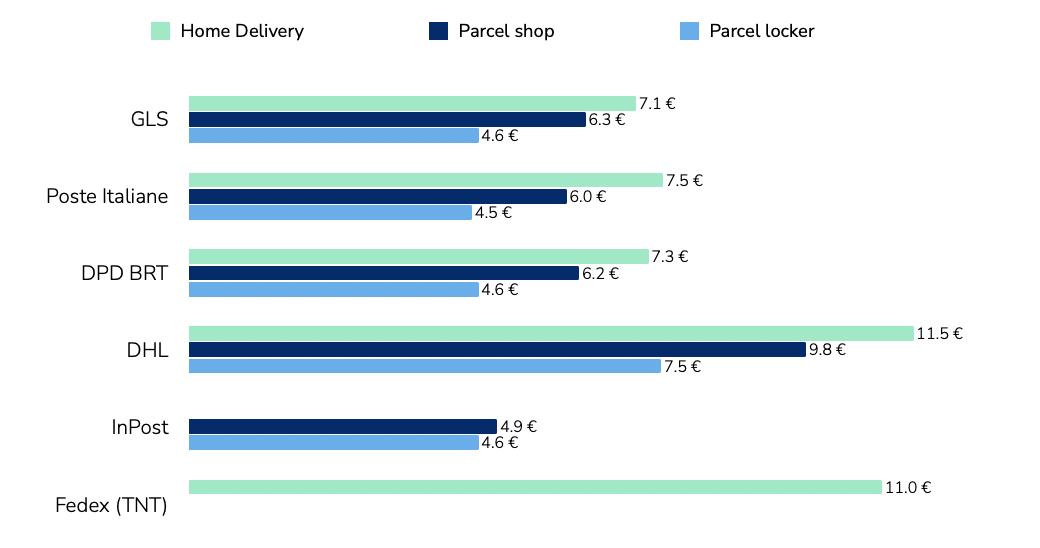

Pricing patterns by method and provider

Pricing across delivery methods follows a clear hierarchy. Home delivery is the most expensive, with DHL and FedEx (TNT) positioned at the higher end in line with their express and international focus.GLS, Poste Italiane, and DPD BRT sit around the market average, reflecting large-scale domestic coverage and standardised pricing structures. InPost maintains the lowest price levels across OOH deliveries, consistent with its parcel-locker model and high network density.

The pricing gap between home and OOH - €6.5 vs €5.8 on average - highlights the economic rationale for providers to keep expanding out-of-home capacity, and in line with most other markets. As networks grow denser, these price differences will continue to influence retailer delivery mix.

Provider portfolios: size mix, categories and growth potential

Tembi’s analysis segments retailer clients by size and growth outlook, showing how each provider’s portfolio is positioned across the Italian market.

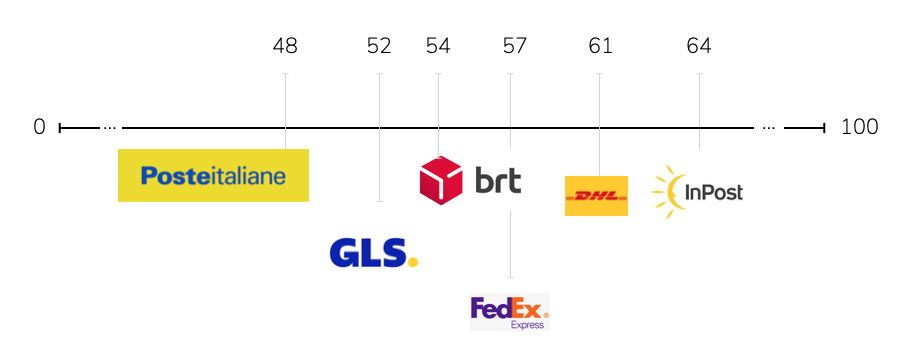

This chart summarises the average retailer size of each provider’s client base on Tembi’s 0–100 scale, where higher scores represent larger and more established webshops.

- Poste Italiane (48) and GLS (52) sit closest to the market average, reflecting broad SMB and national coverage.

- DPD BRT (54) leans slightly higher, showing stronger ties with mid-sized merchants.

- DHL (57), FedEx (61), and InPost (64) serve larger retailers on average - a clear indicator of focus on high-volume or cross-border accounts.

Together, these values illustrate the spectrum from volume-driven national carriers to enterprise-oriented networks.

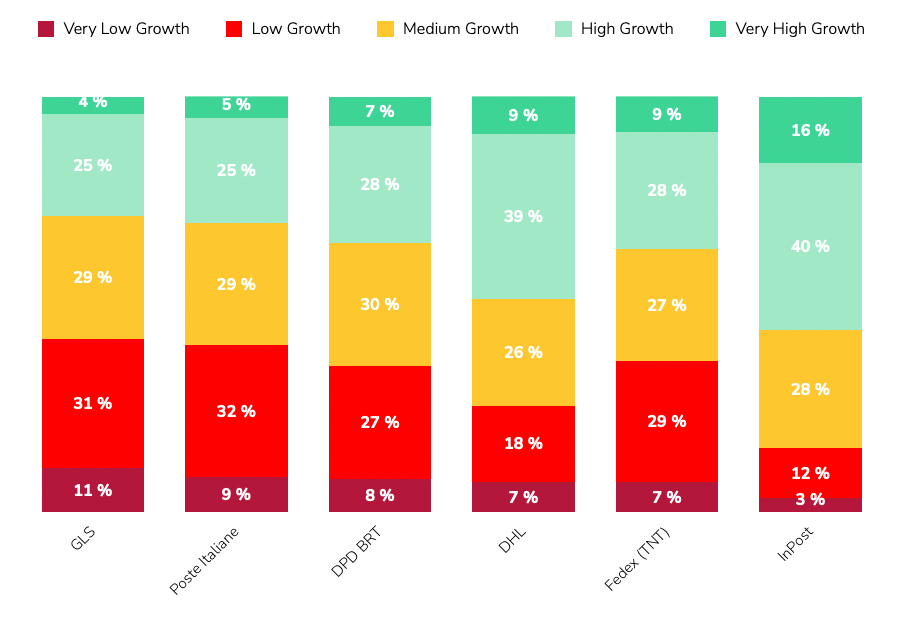

The stacked bars show how each delivery provider’s clients are distributed by retailer size:

- GLS and Poste Italiane have the broadest spread, with roughly two-thirds of their base in small or medium segments.

- DPD BRT follows a similar pattern but with a slightly larger share of large retailers.

- DHL, FedEx (TNT), and InPost have more concentrated portfolios: over half of their clients are categorised as large, and the very large segment grows from 2% for DHL to 4% for InPost.

This pattern shows a clear divide between carriers anchored in national SMB volume and those positioned around larger enterprise webshops.