How the Not-Invented-Here Syndrome can slow you down

In the early 2000s, Open Innovation emerged as a response to the Not-Invented-Here(NIH) Syndrome - a mindset particularly prevalent in engineering and IT organisations.Companies often preferred to build their own solutions rather than adopting existing ones, even when viable alternatives were readily available.

The rise of open innovation, open source, and open data has since accelerated technological progress for everyone. Instead of investing heavily in developing proprietary solutions, businesses can now leverage what already exists, saving time, money, and effort.

Why do companies still build their own solutions?

Despite these advancements, some businesses still choose to develop their own versions of existing solutions. The reasons often include:

- A belief that their needs are unique - assuming no existing solution will fully address their challenges.

- A desire for ownership and control - feeling that an in-house solution offers more flexibility or security.

However, these assumptions often lead to inefficiencies and long-term challenges.

Why reinventing the wheel can be a costly mistake

If a solution already exists in the market, trying to replicate it internally is rarely the best approach. Here’s why:

- Existing solutions are already optimised. Established providers continuously improve their products, meaning businesses benefit from ongoing innovation at a fraction of the cost.

- It’s more cost-effective. The upfront investment has already been made by others, allowing you to buy into a mature solution rather than funding development from scratch.

- Avoiding long-term technical debt. When you build your own solution, you’re responsible for maintenance, updates, and troubleshooting, costs that only increase over time. Dependence on internal teams or external consultants can create bottlenecks and slow progress.

The trap of sunk costs

Once a company has invested in a proprietary solution, it becomes difficult to abandon, even when it’s no longer efficient. This is how businesses end up with a giant with feet of clay, a fragile system that limits agility and innovation.

The Smarter Approach

Rather than building something from the ground up, focus on what differentiates your business. If a solution already exists in the market, build on top of it rather than duplicating efforts. The key to staying competitive isn’t in owning every piece of technology, it’s in leveraging the best tools available to drive your core business forward.

More from

Product

category

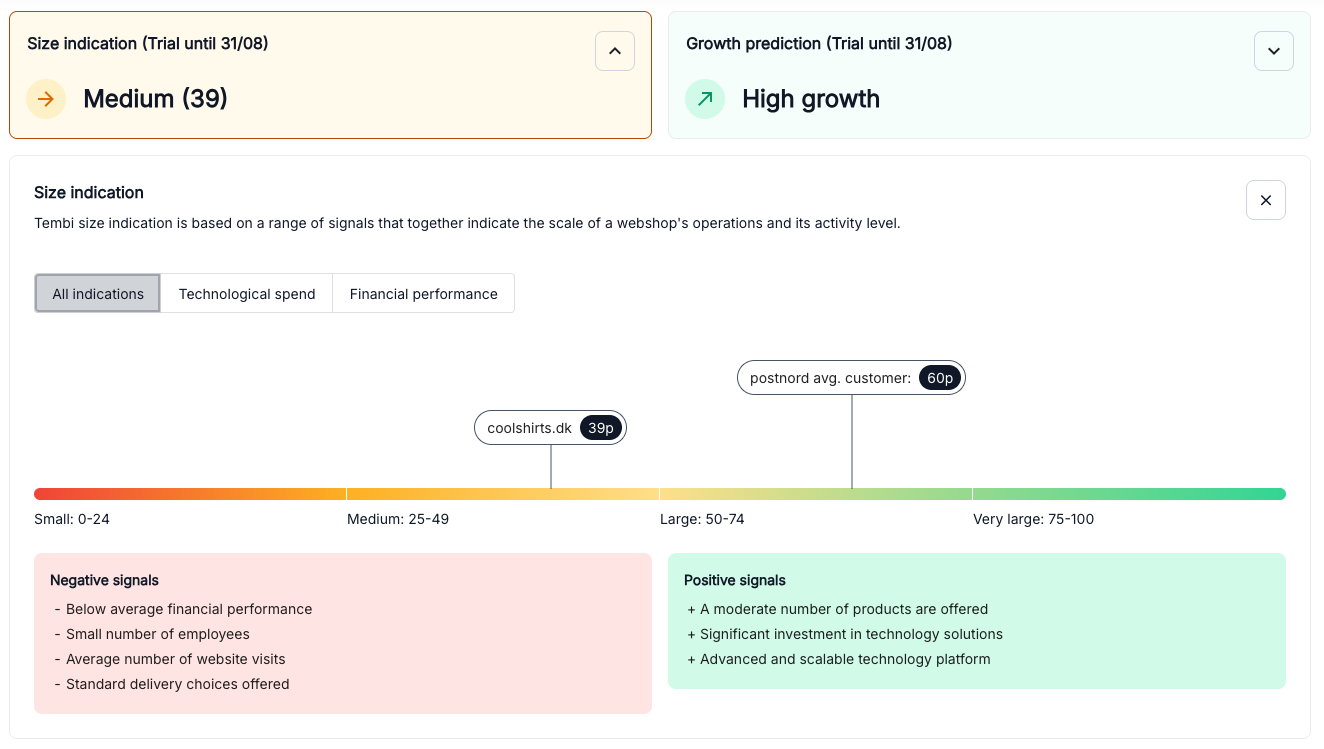

Knowing which webshops to focus on helps your business succeed. That’s why we've launched Tembi’s Size indication, a simple way to quickly understand how active and big (or small) any webshop is in the market compared to the largest online retailers.

What is the Size indication?

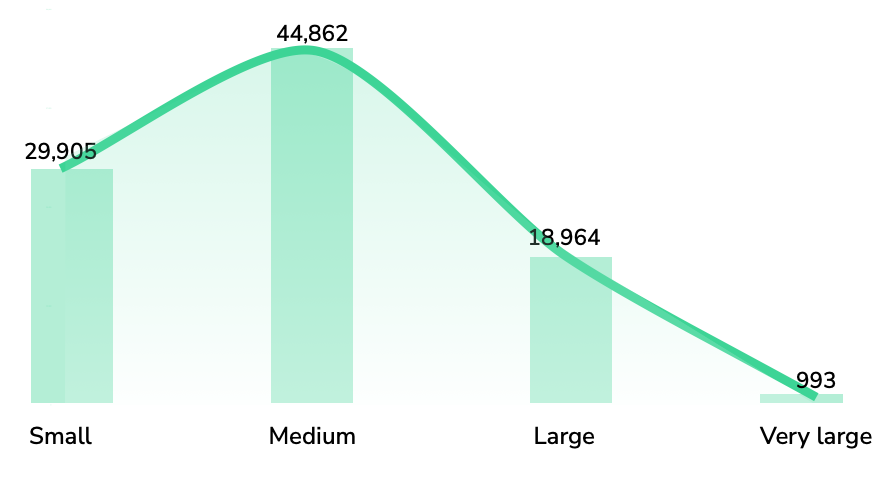

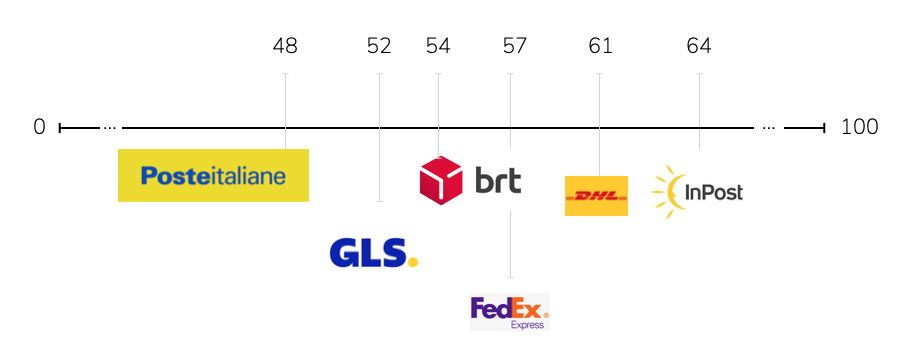

Tembi’s Size indications scores webshops from 1 to 100 points, dividing them into clear groups:

- Small: 0-24 points

- Medium: 25-49 points

- Large: 50-74 points

- Very Large: 75-100 points

This makes it easy to compare webshops and see where they stand compared to others.

How does it work?

The Size indication uses hundreds of data points per webshop to decide each webshop’s score, including:

- Size and variety of product offerings

- Investment in technology and infrastructure

- Amount of website traffic

- Types of delivery methods provided

These factors, and many more, provide a clear picture of how active and large a webshop is. Each webshop’s score is clearly explained, showing both positive and negative factors.

Why the Size indication is useful

The Size indication makes market analysis simpler. You can quickly assess market size and find webshops that fit your ICP. When looking at thousands of prospects, Size indication allows you to sort all webshops, and see their size in relation to each other.

Combine Size indication with Growth Predictions

Tembi’s Size indication works hand-in-hand with our Growth Predictions feature. By combining these insights, you get a complete view of the market opportunity - clearly identifying which webshops are not only large and active but also likely to grow. This powerful combination helps you pinpoint the best opportunities for strategic action and growth.

Want to get started?

Log in to Tembi and check out the Size indication now. All Tembi clients have access to our Growth predictions and Size indication for free during July.

Knowing which webshops to focus on helps your business succeed. That’s why we've launched Tembi’s Size indication, a simple way to quickly understand how active and big (or small) any webshop is in the market compared to the largest online retailers.

What is the Size indication?

Tembi’s Size indications scores webshops from 1 to 100 points, dividing them into clear groups:

- Small: 0-24 points

- Medium: 25-49 points

- Large: 50-74 points

- Very Large: 75-100 points

This makes it easy to compare webshops and see where they stand compared to others.

How does it work?

The Size indication uses hundreds of data points per webshop to decide each webshop’s score, including:

- Size and variety of product offerings

- Investment in technology and infrastructure

- Amount of website traffic

- Types of delivery methods provided

These factors, and many more, provide a clear picture of how active and large a webshop is. Each webshop’s score is clearly explained, showing both positive and negative factors.

Why the Size indication is useful

The Size indication makes market analysis simpler. You can quickly assess market size and find webshops that fit your ICP. When looking at thousands of prospects, Size indication allows you to sort all webshops, and see their size in relation to each other.

Combine Size indication with Growth Predictions

Tembi’s Size indication works hand-in-hand with our Growth Predictions feature. By combining these insights, you get a complete view of the market opportunity - clearly identifying which webshops are not only large and active but also likely to grow. This powerful combination helps you pinpoint the best opportunities for strategic action and growth.

Want to get started?

Log in to Tembi and check out the Size indication now. All Tembi clients have access to our Growth predictions and Size indication for free during July.

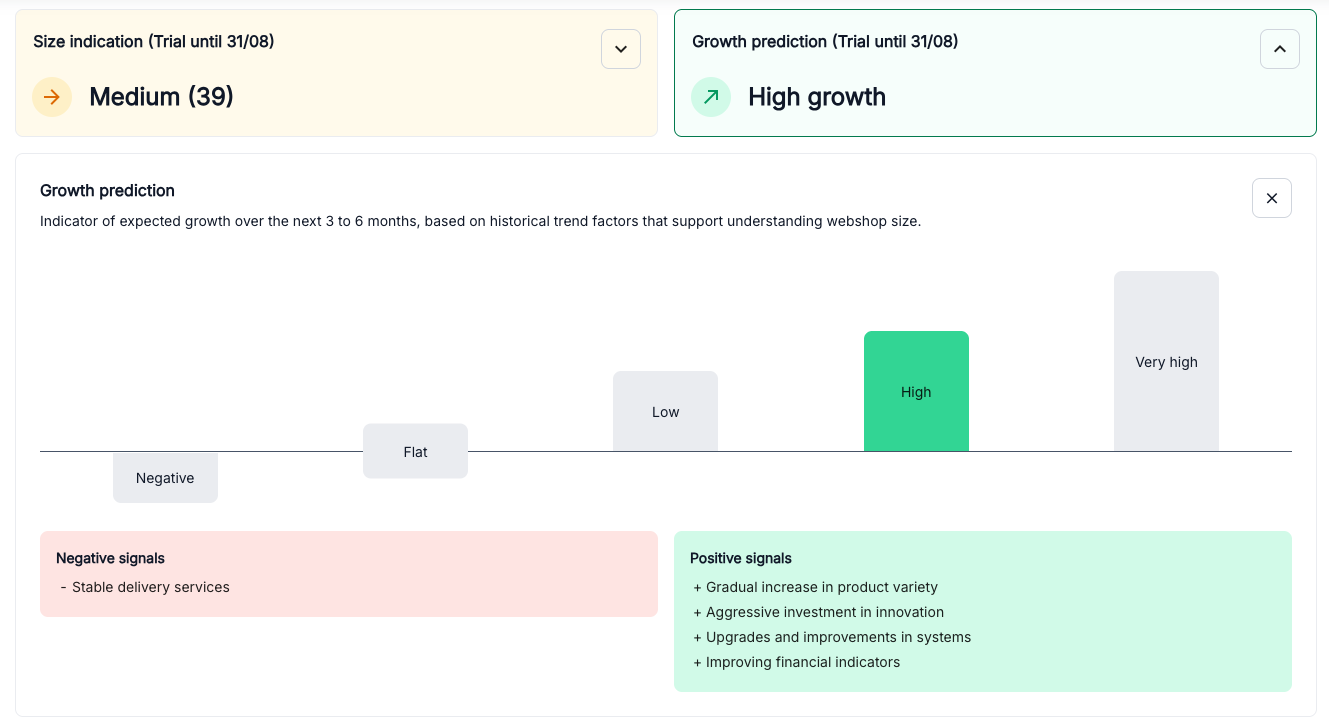

In business, knowledge is power, but foresight is transformational. Until now, most market intelligence relies on delivered reactive insights, offering clarity on the past or present but limited visibility into the future. Today, Tembi changes that by launching a groundbreaking predictive feature for e-commerce: Growth Predictions.

Why predictions matter

Understanding past performance is essential, but knowing what's coming next is where you truly gain a competitive advantage. With Growth Predictions, Tembi analyses hundreds of critical factors across hundreds of thousands of webshops, giving you a clear view of each retailer’s potential growth over the next 3 to 6 months.

How does it work?

Our unique predictive model evaluates comprehensive data points, including:

- Financial trends

- Employee growth and changes

- Product portfolio developments

- Web traffic insights (powered by SimilarWeb)

- Technological investments

- Infrastructure reliability

- Delivery partnerships and methods

- Category-specific trends

At the heart of this model is our proprietary AI-powered data collection methodology. For several years, we've meticulously collected, structured, and continuously updated vast datasets. Our advanced machine-learning algorithms use this rich historical data to identify patterns, learn from past behaviours, and generate precise, data-backed predictions. This ensures that our Growth Predictions aren’t guesses - they're calculated insights driven by robust AI techniques.

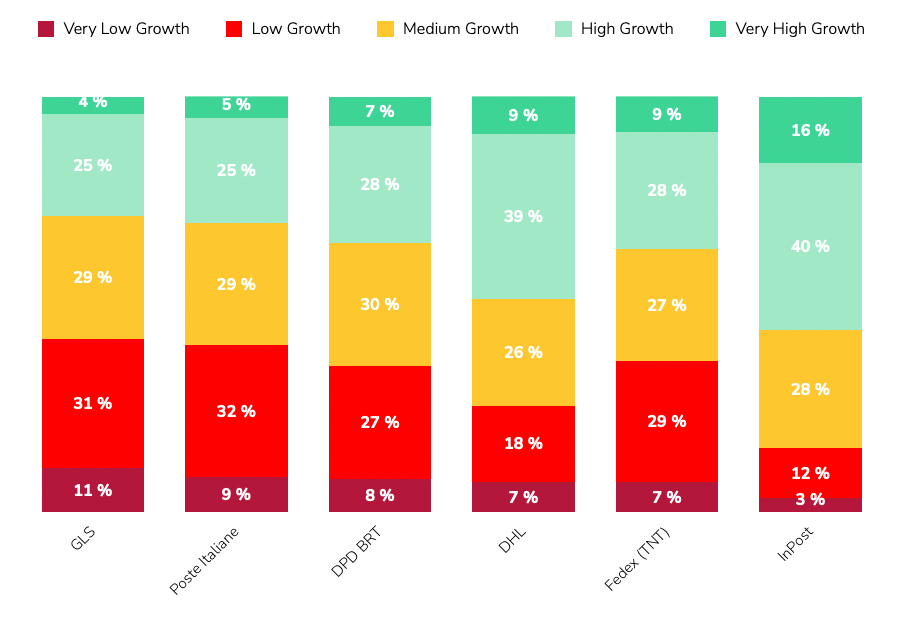

We translate these complex signals into straightforward, actionable insights, predicting whether a webshop will experience high growth, stability, or potential decline.

Transparent insights for smarter decisions

Growth Predictions don't just give you a simple score. They explain precisely why we anticipate certain growth patterns. For example:

- Positive growth signals: Stable infrastructure, Product portfolio expansion, added delivery methods or partners.

- Negative growth signals: Limited product portfolio expansion, insufficient technological investments.

This transparency helps you quickly understand the underlying strengths or vulnerabilities of any webshop.

Transform your commercial strategies

If you’re responsible for partnerships, sales, or logistics, Growth Predictions become your secret weapon. Prioritise your efforts, target the right segments and customers, optimise your resources, and proactively manage your commercial relationships by focusing on webshops that have a higher likeability to succeed.

First of its kind

No other e-commerce intelligence tool provides predictive growth insights at this depth. Using our unique dataset of retailers and product portfolios, we provide a comprehensive mapping of the e-commerce industry, helping companies plan strategically.

We update our dataset bi-weekly, ensuring teams can track prospects, provide insights and get a competitive advantage.

Interested in knowing more, book a demo with one of our experts.

Growth predictions are available for free as an early release during July for all our clients.

In business, knowledge is power, but foresight is transformational. Until now, most market intelligence relies on delivered reactive insights, offering clarity on the past or present but limited visibility into the future. Today, Tembi changes that by launching a groundbreaking predictive feature for e-commerce: Growth Predictions.

Why predictions matter

Understanding past performance is essential, but knowing what's coming next is where you truly gain a competitive advantage. With Growth Predictions, Tembi analyses hundreds of critical factors across hundreds of thousands of webshops, giving you a clear view of each retailer’s potential growth over the next 3 to 6 months.

How does it work?

Our unique predictive model evaluates comprehensive data points, including:

- Financial trends

- Employee growth and changes

- Product portfolio developments

- Web traffic insights (powered by SimilarWeb)

- Technological investments

- Infrastructure reliability

- Delivery partnerships and methods

- Category-specific trends

At the heart of this model is our proprietary AI-powered data collection methodology. For several years, we've meticulously collected, structured, and continuously updated vast datasets. Our advanced machine-learning algorithms use this rich historical data to identify patterns, learn from past behaviours, and generate precise, data-backed predictions. This ensures that our Growth Predictions aren’t guesses - they're calculated insights driven by robust AI techniques.

We translate these complex signals into straightforward, actionable insights, predicting whether a webshop will experience high growth, stability, or potential decline.

Transparent insights for smarter decisions

Growth Predictions don't just give you a simple score. They explain precisely why we anticipate certain growth patterns. For example:

- Positive growth signals: Stable infrastructure, Product portfolio expansion, added delivery methods or partners.

- Negative growth signals: Limited product portfolio expansion, insufficient technological investments.

This transparency helps you quickly understand the underlying strengths or vulnerabilities of any webshop.

Transform your commercial strategies

If you’re responsible for partnerships, sales, or logistics, Growth Predictions become your secret weapon. Prioritise your efforts, target the right segments and customers, optimise your resources, and proactively manage your commercial relationships by focusing on webshops that have a higher likeability to succeed.

First of its kind

No other e-commerce intelligence tool provides predictive growth insights at this depth. Using our unique dataset of retailers and product portfolios, we provide a comprehensive mapping of the e-commerce industry, helping companies plan strategically.

We update our dataset bi-weekly, ensuring teams can track prospects, provide insights and get a competitive advantage.

Interested in knowing more, book a demo with one of our experts.

Growth predictions are available for free as an early release during July for all our clients.

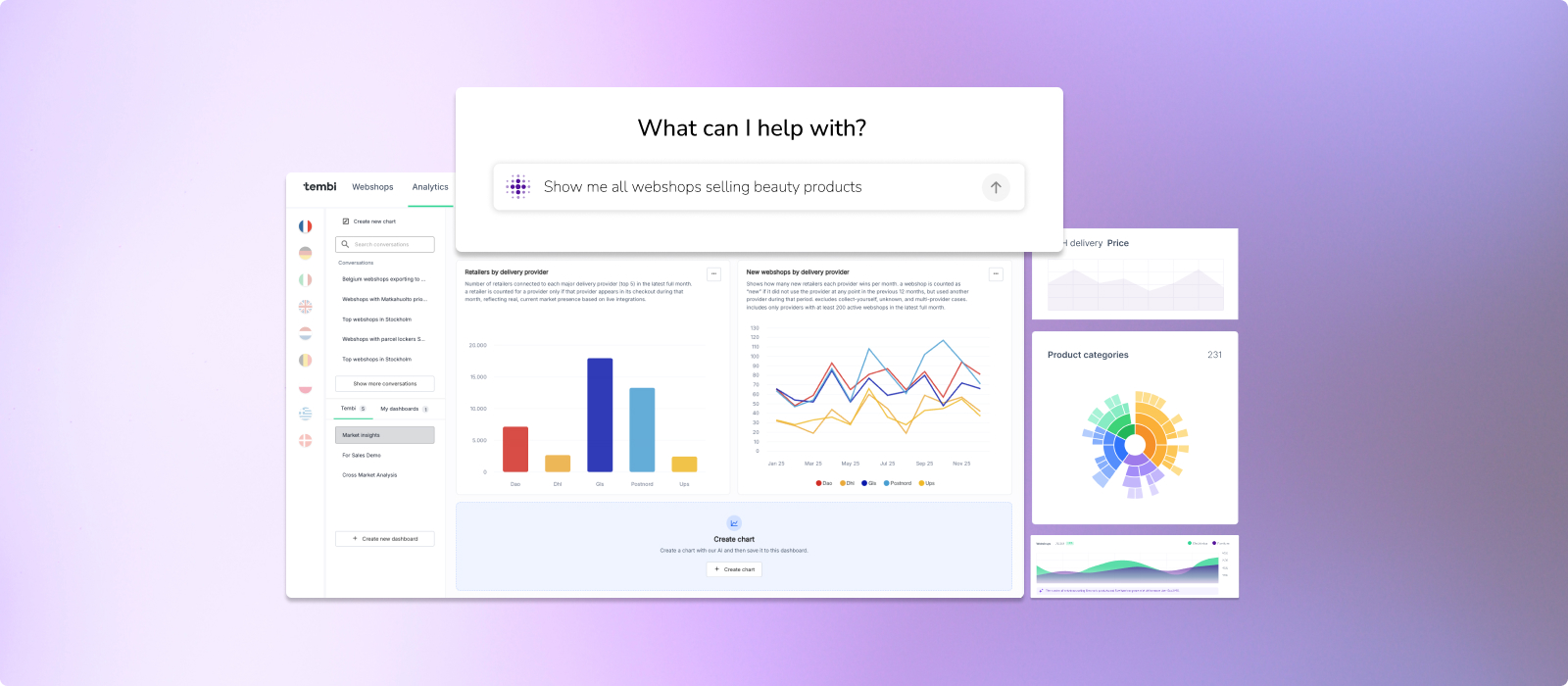

Today we’re rolling out Product Insights – a new tool that instantly breaks down the product catalogue of almost any webshop. By continuously monitoring 600,000 webshops and over 300 million products, Product Insights helps users find answers to questions that used to take days of manual work.

Understanding a retailer's product portfolio has always been a challenge – especially at scale. Tembi’s Product Insights structures each webshop’s catalogue based on Google’s product taxonomy (with over 2,000 sub-categories). Select a category, explore which sub-categories are sold, and get a clear view of the retailer’s product strategy.

Product Insights also lets you track trends over time. What categories are growing? Which brands are expanding? What product types are being phased out? With bi-weekly updates, your market understanding becomes sharper, faster, and far more granular than ever before.

Track product portfolio development

See exactly which brands a webshop sells, the total number of SKUs, and how they’re distributed across product categories. Our time-series view lets you pinpoint when a retailer expands or trims its range – whether that means adding 50 new kitchen appliances in March or dropping three footwear brands in May. Drill down by category or brand to understand growth spurts, assortment gaps, and strategic shifts at a glance.

Product weight and dimensions

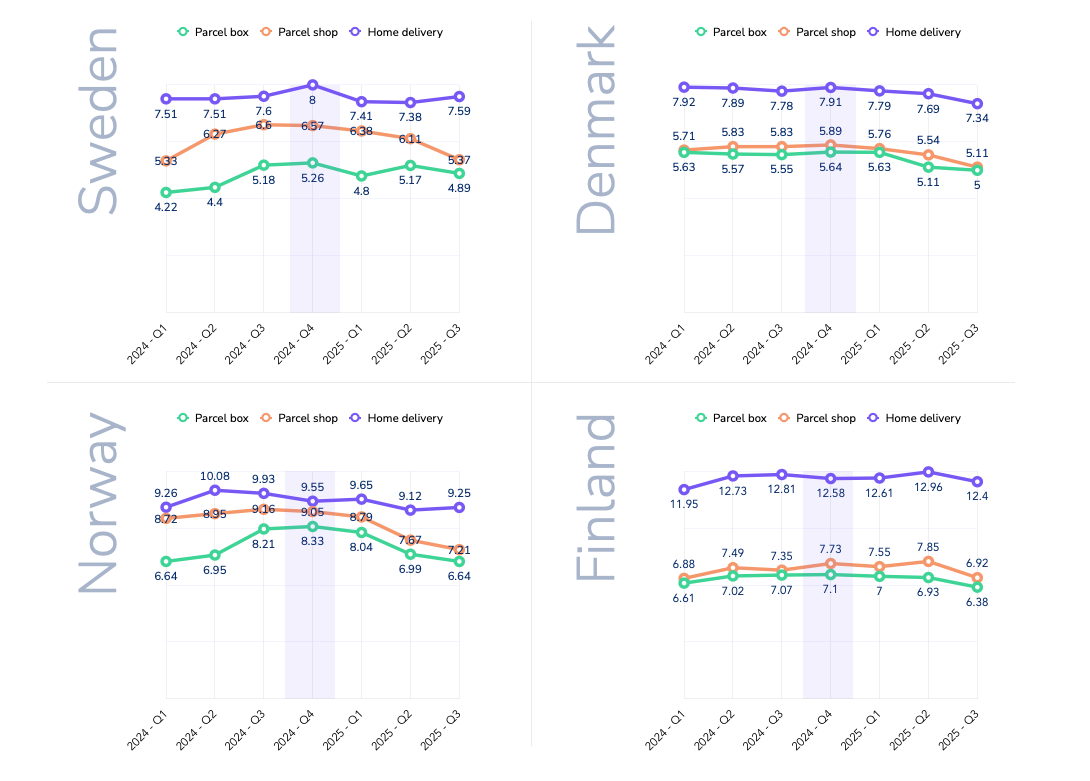

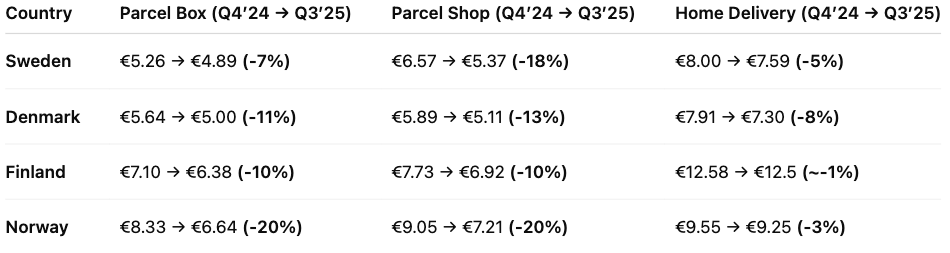

Visualise a webshop’s entire catalogue by weight and dimensions in one interactive chart. The horizontal axis splits product prices into six bands; the vertical axis divides weights into six ranges. Each bubble’s size shows how many items fall into that combined bracket.

Track market trends

Go beyond individual retailers and tap into broader market movements. With Product Insights, you can zoom out and analyse how categories, brands, and product types are evolving across the entire e-commerce landscape in Europe (18 markets).

See which product categories are gaining momentum, what brands are expanding their reach, and how average product sizes or prices are shifting. Filter by country, industry or platform to spot changes in consumer demand, pricing trends, or assortment strategies.

Whether you're a brand manager trying to spot gaps, a logistics provider tracking shipping implications, or a buyer evaluating sourcing decisions – Product Insights turns market noise into clear, structured signals.

Discover and benchmark similar webshops

Instantly compare any retailer with others and uncover new prospects. Tembi’s Similar Webshops feature identifies other webshops with matching assortment structures, traffic levels, and category focus.

It’s a fast way to benchmark a client against competitors – or to find high-potential leads you might otherwise miss. Want to compare delivery providers across similar stores? Or find out how two apparel retailers differ in average price point and category spread? Just click “Full comparison” and dive into the details.

You can also scan for rising players in your segment. Use Similar Webshops to uncover up-and-coming stores with fast-growing assortments – perfect for partnership, outreach, or competitive monitoring.

Start exploring tomorrow

Product Insights is available now on Tembi. Whether you're tracking competitors, mapping out market shifts or sourcing prospects – the data you need is finally structured, searchable, and updated every two weeks.

Want to know more? Book a demo today!

Today we’re rolling out Product Insights – a new tool that instantly breaks down the product catalogue of almost any webshop. By continuously monitoring 600,000 webshops and over 300 million products, Product Insights helps users find answers to questions that used to take days of manual work.

Understanding a retailer's product portfolio has always been a challenge – especially at scale. Tembi’s Product Insights structures each webshop’s catalogue based on Google’s product taxonomy (with over 2,000 sub-categories). Select a category, explore which sub-categories are sold, and get a clear view of the retailer’s product strategy.

Product Insights also lets you track trends over time. What categories are growing? Which brands are expanding? What product types are being phased out? With bi-weekly updates, your market understanding becomes sharper, faster, and far more granular than ever before.

Track product portfolio development

See exactly which brands a webshop sells, the total number of SKUs, and how they’re distributed across product categories. Our time-series view lets you pinpoint when a retailer expands or trims its range – whether that means adding 50 new kitchen appliances in March or dropping three footwear brands in May. Drill down by category or brand to understand growth spurts, assortment gaps, and strategic shifts at a glance.

Product weight and dimensions

Visualise a webshop’s entire catalogue by weight and dimensions in one interactive chart. The horizontal axis splits product prices into six bands; the vertical axis divides weights into six ranges. Each bubble’s size shows how many items fall into that combined bracket.

Track market trends

Go beyond individual retailers and tap into broader market movements. With Product Insights, you can zoom out and analyse how categories, brands, and product types are evolving across the entire e-commerce landscape in Europe (18 markets).

See which product categories are gaining momentum, what brands are expanding their reach, and how average product sizes or prices are shifting. Filter by country, industry or platform to spot changes in consumer demand, pricing trends, or assortment strategies.

Whether you're a brand manager trying to spot gaps, a logistics provider tracking shipping implications, or a buyer evaluating sourcing decisions – Product Insights turns market noise into clear, structured signals.

Discover and benchmark similar webshops

Instantly compare any retailer with others and uncover new prospects. Tembi’s Similar Webshops feature identifies other webshops with matching assortment structures, traffic levels, and category focus.

It’s a fast way to benchmark a client against competitors – or to find high-potential leads you might otherwise miss. Want to compare delivery providers across similar stores? Or find out how two apparel retailers differ in average price point and category spread? Just click “Full comparison” and dive into the details.

You can also scan for rising players in your segment. Use Similar Webshops to uncover up-and-coming stores with fast-growing assortments – perfect for partnership, outreach, or competitive monitoring.

Start exploring tomorrow

Product Insights is available now on Tembi. Whether you're tracking competitors, mapping out market shifts or sourcing prospects – the data you need is finally structured, searchable, and updated every two weeks.

Want to know more? Book a demo today!

s the Swedish real estate market continues to evolve, new trends are emerging, particularly within the commercial sector. Our latest Market Intelligence Report offers an in-depth look into these shifts, providing deep insights and predictions for 2024that could help the industry better understand the market. And where to look for opportunities.

The past six months we have seen a significant activity within the Swedish commercial real estate scene. Over 3,005 companies, each with more than five employees, have relocated, showcasing a trend that follows previous years patterns. Notably, businesses ranging from 5 to 9 employees formed the majority of these moves, highlighting a high activity within this segment.

The Predictive pulse of 2024

Looking ahead, our analytical models have identified a high relocation indicator for 4,698 companies having more than five employees. This indication, drawn from AI models and extensive market data, suggests an active year with a lot of potential. Interestingly, the bulk of this movement is expected from companies with 10 to 49 employees, pointing to a important reshuffling in the commercial real estate space.

Regional Revelations

The report sheds light on the geographical nuances of these relocations. While the Stockholm region has traditionally been a hub of activity, the forthcoming year places a spotlight on Gothenburg, anticipating a higher volume of larger entities on the move. This regional redistribution of commercial real estate activity underscores the diverse opportunities unfolding across Sweden.

In light of that, we also see that companies and production units with more than 20employees in Stockholm tend to move more often than in other parts of the country. 33% of companies in Stockholm changed address during the last three years, while the same number in Gothenburg is 27%.

The Industries on the Move

Diving deeper, certain industries emerge as more mobile than others, including sectors like insurance, information services, and staffing solutions.

Why This Matters

For businesses and investors, understanding these patterns is crucial. The shifting sands of the commercial real estate market offer both challenges and opportunities. For investors, it's a chance to anticipate demand in growing areas and sectors. For businesses, the insights provide a roadmap for strategic decisions about where to plant their flags in a competitive landscape.

Access the full report by clicking on the picture below

s the Swedish real estate market continues to evolve, new trends are emerging, particularly within the commercial sector. Our latest Market Intelligence Report offers an in-depth look into these shifts, providing deep insights and predictions for 2024that could help the industry better understand the market. And where to look for opportunities.

The past six months we have seen a significant activity within the Swedish commercial real estate scene. Over 3,005 companies, each with more than five employees, have relocated, showcasing a trend that follows previous years patterns. Notably, businesses ranging from 5 to 9 employees formed the majority of these moves, highlighting a high activity within this segment.

The Predictive pulse of 2024

Looking ahead, our analytical models have identified a high relocation indicator for 4,698 companies having more than five employees. This indication, drawn from AI models and extensive market data, suggests an active year with a lot of potential. Interestingly, the bulk of this movement is expected from companies with 10 to 49 employees, pointing to a important reshuffling in the commercial real estate space.

Regional Revelations

The report sheds light on the geographical nuances of these relocations. While the Stockholm region has traditionally been a hub of activity, the forthcoming year places a spotlight on Gothenburg, anticipating a higher volume of larger entities on the move. This regional redistribution of commercial real estate activity underscores the diverse opportunities unfolding across Sweden.

In light of that, we also see that companies and production units with more than 20employees in Stockholm tend to move more often than in other parts of the country. 33% of companies in Stockholm changed address during the last three years, while the same number in Gothenburg is 27%.

The Industries on the Move

Diving deeper, certain industries emerge as more mobile than others, including sectors like insurance, information services, and staffing solutions.

Why This Matters

For businesses and investors, understanding these patterns is crucial. The shifting sands of the commercial real estate market offer both challenges and opportunities. For investors, it's a chance to anticipate demand in growing areas and sectors. For businesses, the insights provide a roadmap for strategic decisions about where to plant their flags in a competitive landscape.

Access the full report by clicking on the picture below

.png)